The One Gap That Changes Your Financial Life

Debt has a way of making life feel smaller. Fewer choices. Fewer options. Less breathing room. I’ve lived that tight-chested season, and I can tell you this: paying off debt is powerful, but it’s not the whole story. Real peace comes from building a financial freedom gap… the space between what you earn and what you spend. That gap is where confidence lives.

If you’ve ever been in serious debt, or are right now, you know the feeling that your creditors own you lock, stock, and bank account. I’ve been there. Debt steals your freedom one option at a time until you become its prisoner.

Debt keeps you chained to a job you hate. It keeps you stuck in the past, unable to move forward. And big debt causes terrible stress that makes it hard to breathe, keeps you awake, spoils relationships, and zaps the joy out of living.

It makes sense that if debt steals your options, then repaying debt creates financial freedom. But that’s not necessarily true.

If you spend just the amount you earn, you won’t be creating new debt, but you will be broke at the end of every month, spinning your wheels and living paycheck to paycheck. That’s not freedom. That’s survival.

What Is a Financial Freedom Gap?

The first rule of sound money management is to live below your means… spend less than you earn. This means creating a margin between what you earn and what you spend. The secret to finding financial freedom, freedom from financial worry, fear and want, is the gap between the amount you earn and your spending.

The wider the gap, the more freedom you will enjoy. The money you don’t spend gives you the freedom to grow your dreams and prepare for the future.

There’s a difference between being debt-free and being financially free. One removes a burden. The other builds breathing room.

The real shift happens when you create a financial freedom gap, the margin between what you earn and what you spend. That space is what lets you sleep better, make choices without panic, and fund the life you actually want.

How to Widen Your Financial Freedom Gap

There are two ways to increase the space between what you earn and what you spend:

- Spend less

- Earn more

The harder you work at doing either (or both) the more successful you’ll be in finding financial freedom: freedom to fund your children’s education, freedom to travel, to invest, to relocate, to retire… freedom to live the life you love.

It’s not flashy. It’s not complicated. Spend a little less. Earn a little more. Plug the leaks. Repeat.

Practical Ways to Spend Less Without Feeling Deprived

Spending less sounds easy, doesn’t it? If it were, we wouldn’t have crossed $5.1 trillion in total consumer credit outstanding at the end of 2025.

In 2025 alone, consumer credit increased 2.4 percent. Revolving credit, mostly credit cards, rose 3.4 percent. And in December, revolving balances jumped at a 12.6 percent annual rate. Translation? Even with higher interest rates, we’re still leaning hard on plastic.

And that plastic is expensive. The average credit card APR is hovering around 21%. New car loans are still above 7% at many banks. When borrowing costs that much, every dollar you don’t spend earns you a guaranteed return equal to the interest you’re not paying.

Spending less takes intention, but it’s still the fastest way to change your financial situation. You’ve already earned the money and paid taxes on it. There’s no application process. No approval. No waiting.

Here’s how to do it in a way that builds freedom without making life miserable.

Get Serious

Vague goals don’t move the needle. “I’ll try to spend less” won’t cut it.

Put it in writing. Decide how much you want to reduce your monthly spending and exactly where it will come from. Then “pre-spend” your income on paper before you spend it in real life… also known as a budget.

In a world of tap-to-pay and one-click checkout, awareness is power. If you don’t tell your money where to go, it will quietly disappear.

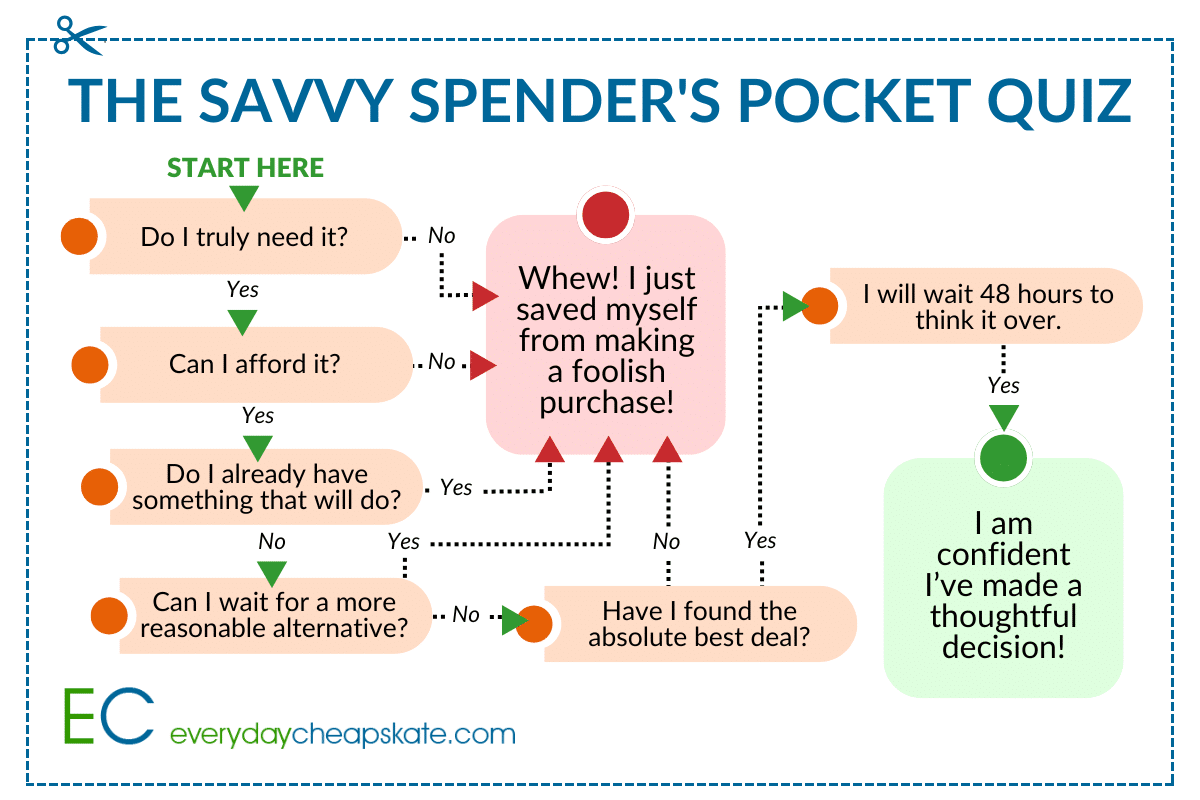

Use a 60-Second Spending Filter

Before spending more than $20, pause and ask:

- Do I need it?

- Do I already have something that will work?

- Do I need it right now or can it wait?

- Have I found the best value?

With credit card rates above 20%, that impulse purchase isn’t just $40. If it rides a balance, it could easily become $50 or $60 over time. One honest “No” is your cue to walk away.

Reinstate the Waiting Rule

In the age of same-day delivery, waiting feels radical. That’s exactly why it works.

Impose a 24-hour rule for non-essential purchases. Add it to your cart if you must, but don’t check out. Most of the time, the urgency fades. Sometimes you forget entirely. That’s not deprivation. That’s clarity.

Smart Ways to Earn More

Cutting expenses creates quick wins. But earning more? That’s where your gap can really widen.

Yes, it takes more effort. But increasing income gives you leverage.

Here are realistic ways to do it without burning out.

Increase Hours

If overtime or extra shifts are available, consider a short sprint. Even 5–10 extra hours a week for a few months can knock out a credit card balance or boost your emergency fund.

If traditional overtime isn’t an option, ask about project-based bonuses or performance incentives. Companies are often more flexible than we assume, especially when you come prepared.

Improve a Skill

You don’t necessarily need another degree. You need a skill the market values.

Think digital skills (AI tools, bookkeeping software, social media management), technical trades, tutoring, coaching, or specialized repair work. Short certification programs, many online and affordable, can position you for higher-paying work faster than you think.

The goal isn’t to collect credentials. It’s to increase your earning power.

Moonlight

Not forever. Just long enough to create breathing room.

Seasonal retail, tax-season prep work, event staffing, delivery driving, or short-term contract projects can provide a focused income boost. A defined start and stop date keeps it sustainable.

A temporary push now can prevent long-term stress later.

Freelance

The freelance world has evolved. Businesses increasingly hire contract talent instead of full-time staff.

If you write, design, edit, code, manage social media, organize data, or handle bookkeeping, there’s demand. Platforms have changed over the years, but the opportunity hasn’t. Many freelancers now build income through direct outreach, LinkedIn networking, and small business referrals rather than relying solely on bidding sites.

And yes, AI tools can help you work faster and increase your output without increasing your hours.

Rent What You’re Not Using

Unused space is idle income.

Garage storage. Parking space. A spare room. Even equipment (tools, cameras, specialty gear) can be rented locally. In many communities, peer-to-peer rental platforms make this easier than ever.

You don’t need to become a landlord. Just look at what’s sitting unused.

Turn Knowledge Into Income

You don’t have to be a professor to teach.

Tutoring (in person or online), coaching, consulting in your field, teaching a workshop at a community center, or creating a simple digital guide can turn experience into income. In a world that values flexibility and remote access, knowledge scales.

If someone regularly asks you for advice, there may be income potential there.

Ask for the Raise (With Data)

Wages have shifted in many industries over the last few years. If you haven’t evaluated your compensation recently, it may be time.

Document your contributions. Quantify your results. Research market rates. Then ask.

You don’t need to demand. You need to demonstrate value.

Strengthen Your Network

Opportunities still flow through relationships.

Let people know what you’re capable of. Update your LinkedIn. Reconnect with former colleagues. Attend one local event. Mention your side skills in conversation.

Visibility matters. If people don’t know you’re available, they can’t refer you.

Plug the Leaks That Shrink Your Gap

Start paying attention to where money quietly drains away. Look at everything from excessive electricity and water usage to overpaying for insurance.

Frugality simply means maximizing every dollar so you stop wasting money and start funding your gap. Set your own standards. You don’t need to do anything that makes you uncomfortable, but you do need to pay attention.

Cancel What You’re Not Using

Subscriptions are still one of the biggest silent drains and they’ve gotten sneakier.

Streaming platforms, AI tools, cloud storage upgrades, fitness apps, meal kits, subscription boxes, auto-renew warranties. Many come with price increases after “intro” periods.

Here’s a simple quarterly habit:

- Open your bank and credit card statements.

- Highlight every recurring charge.

- Ask one question: Would I sign up for this again today at this price?

- If the answer is no, cancel it.

Even trimming $50 a month creates $600 a year in breathing room. That’s a car repair fund. A weekend getaway. A starter emergency cushion.

Cook More, Stress Less, Save More

Look at how much you’re spending on food outside the home at restaurants, drive-thrus, coffee shops. It adds up quickly.

Learning to cook at home can turn a $90-$120 restaurant meal for four into a satisfying $15 home meal with leftovers. Think:

- Breakfast for dinner

- Big-batch soup (freezer-friendly and comforting)

- Sheet pan meals

- Slow cooker staples

That difference goes straight into your gap without sacrificing comfort.

Watch the Utility Creep

Utility costs fluctuate more than they used to. Electricity, water, and gas rates vary seasonally and regionally. Small shifts matter:

- Adjust the thermostat 1–2 degrees.

- Seal drafty windows.

- Run full loads only.

- Switch to LED if you still have older bulbs lingering.

It’s not glamorous, but steady awareness prevents surprise spikes.

Insurance and Services Checkup

Auto and home insurance rates have risen in many areas. If you haven’t compared quotes in the past year, you could be overpaying without realizing it. Set a reminder once a year to:

- Request updated quotes.

- Revisit deductibles.

- Ask about discounts (bundling, safe driving, loyalty).

Five phone calls could mean hundreds saved.

Make Frugality a Personal Challenge

Instead of framing frugality as restriction, turn it into a creative exercise.

- Stretch groceries from 7 days to 10.

- Delay replacing something and repair it first.

- See how long you can go without buying anything non-essential.

Not to deprive yourself, but to strengthen your resourcefulness muscle. You may discover that what you really needed wasn’t more income.

It was simply a little more intention.

Build Margin for the Life You Actually Want

Resources are waiting for you… books, archives, daily encouragement. Surround yourself with reminders that this is possible.

I’ve been on both sides of this, and I promise: margin changes everything.

Start small. Start today. Your future self will thank you.

Question: What’s one simple change you’ve made that widened the gap between what you earn and what you spend? Share in the comments below.

EverydayCheapskate™ is reader-supported. We participate in the Amazon Services LLC Associates Program and other affiliate advertising programs, designed to provide a means for us to earn from qualifying purchases, at no cost to you.

More from Everyday Cheapskate

https://www.everydaycheapskate.com/wp-content/uploads/20260715-high-yield-savings-account-man-dropping-quarter-into-mason-jar.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-15 18:01:312026-07-15 18:01:31The Boring Money Move That Earns You $400 to $2,000 a Year (High-Yield Savings Explained)

https://www.everydaycheapskate.com/wp-content/uploads/20260715-high-yield-savings-account-man-dropping-quarter-into-mason-jar.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-15 18:01:312026-07-15 18:01:31The Boring Money Move That Earns You $400 to $2,000 a Year (High-Yield Savings Explained) https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should) https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies)

https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies) https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50%

https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50% https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days

https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom

https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom https://www.everydaycheapskate.com/wp-content/uploads/20260703-home-decor.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-03 20:46:552026-07-03 20:46:5510 Everyday Items You Never Think to Wash (But Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260703-home-decor.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-03 20:46:552026-07-03 20:46:5510 Everyday Items You Never Think to Wash (But Should) https://www.everydaycheapskate.com/wp-content/uploads/20260630-a-lit-sparkler-with-an-american-flag-in-the-background-4th-of-july-hacks-tips-and-recipes.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-30 21:44:502026-06-30 21:44:5034 Fourth of July Recipes and DIY Hacks for a Stress-Free Holiday

https://www.everydaycheapskate.com/wp-content/uploads/20260630-a-lit-sparkler-with-an-american-flag-in-the-background-4th-of-july-hacks-tips-and-recipes.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-30 21:44:502026-06-30 21:44:5034 Fourth of July Recipes and DIY Hacks for a Stress-Free Holiday https://www.everydaycheapskate.com/wp-content/uploads/20260629-wooden-die-spell-july-with-patriotic-decor-in-background.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-29 21:07:092026-06-29 21:10:297 Best Things to Buy in July for Huge Summer Savings

https://www.everydaycheapskate.com/wp-content/uploads/20260629-wooden-die-spell-july-with-patriotic-decor-in-background.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-29 21:07:092026-06-29 21:10:297 Best Things to Buy in July for Huge Summer Savings

HI i have written before regarding my financial delemma but hadn’t heard anything. I am 77 and over the years have used my credit cards to help family. my credit cards are high and with the rates going up I am trying to get some help. banks won’t help, and i’m not sure about debt consolidation, not relief, my score is 651. i stay awake at nites trying to think of ways, sell furniture etc. where else can i go. my brother is in nursing home and i have his dog whicch is another bill. I need to get help with the credit card amt so i can have money freed up to get a facial and do something for me. thank you

Go to NFCC.org immediately. Or if you prefer, call NFCC at 800-388-2227. You have a difficult situation, Teresa and one created out of your desire to help others before you were financially secure. Going into debt to help relatives because you do not have the money in hand to do that may see like a kind and caring thing to do, but it’s like trying to rescue a drowning person when you don’t know how to swim. Both of you will likely drown. That may sound harsh, but it’s time to face the truth. Without dobut, you will have to make some difficult decisions going forward. I hope you will make that call as soon as possible. These are good people at NFCC and they can help. You can trust them. I wish you well!

Wood home furniture has something quite natural about it. There is this feeling of warmth,

of attribute and also of style that may be be discovered in wood furnishings.

Hardwood is actually born coming from the earth.

It seems like I chime in every time Mary posts something like this to second her advice. I learned to live below my means (partly accident and partly by design) when I was just starting out. I perfected it when I was poor and I continue it now that I’m doing better and earning more than ever before. I’ve followed this path and although I’m not wealthy, I have Financial freedom and peace of mind. It really is as simple as live below your means. One big tip I’ll add to Mary’s list is to consider purchases in terms of how many hours you’ll work to pay for them. Two hours (or more) of work for a meal out (and not even a really nice one) makes the idea much less appealing. You’ll find your impulse buys pretty much disappear and you won’t miss them.