The Top Credit Card Debt Questions Readers Ask

If you could peek inside my inbox, you might expect questions about laundry mishaps or bargain finds, and yes, those show up. But the questions that never stop coming are about credit cards and debt. Not theory. Not hypotheticals. Real-life “What should I do right now?” questions. I don’t offer credentials or fancy charts… just lessons learned the hard way, and answers I wish someone had given me sooner.

If you were to dive into my inbox, you might assume it’s packed with questions about laundry mishaps, copycat recipes, or the best inexpensive version of whatever’s trending this week. And yes, those absolutely show up. But the questions that rise to the top again and again are about credit cards and consumer debt. That topic wins by a landslide.

You might find that surprising, since I’m not a financial planner or investment advisor. I don’t hold licenses, certifications, or fancy credentials. What I do have is lived experience… and plenty of it. The kind you earn the hard way and never forget.

There was a time when I owned 35 credit cards. All at once. I also leased more than my share of new cars (not all at the same time, thankfully). I hit bottom, flailed hard to stay afloat, and eventually clawed my way out of the mess. Today, I live completely debt-free. And no, it didn’t happen by accident.

Recent data from the Federal Reserve Bank of New York shows household debt in the U.S. has climbed to a new all-time high, with credit card balances right there in the mix. Credit card debt alone just crossed the $1.2 trillion mark. That tells me what readers already know: a lot of everyday expenses are being charged, carried, and worried over. This isn’t an edge case. It’s normal life right now.

My journey taught me lessons no textbook or economic report ever could. What follows are the questions readers ask me most often, along with my honest answers. These are my opinions, shaped by mistakes, persistence, and results. Take what fits your life, leave what doesn’t, and use it to make your next decision a smarter one.

Why Home Equity and Credit Cards Don’t Mix

Q: Should I take a home equity loan to pay off my credit cards?

A: No. And the clearest way to understand why is to walk through the worst-case scenario. Always ask yourself this first: What happens if I can’t make the payments?

If you default on a credit card, the damage is real… fees, penalties, and a bruised credit report. But the bank cannot take your house. That matters. When you move unsecured credit card debt onto your home through a home equity loan, you change the stakes entirely. If you hit financial trouble after that, you’re no longer risking your credit. You’re risking your address. And yes, you could end up on the street with your recliner.

Defaulting on a home equity loan leads to foreclosure. But the real loss goes deeper than that. Your home equity is an appreciating asset. Left alone and allowed to grow, it moves you closer to owning your home outright.

That future never arrives if you treat your equity like an ATM or a hidden savings account. Once you spend it, it’s gone and rebuilding it is far harder than running up a credit card balance ever was.

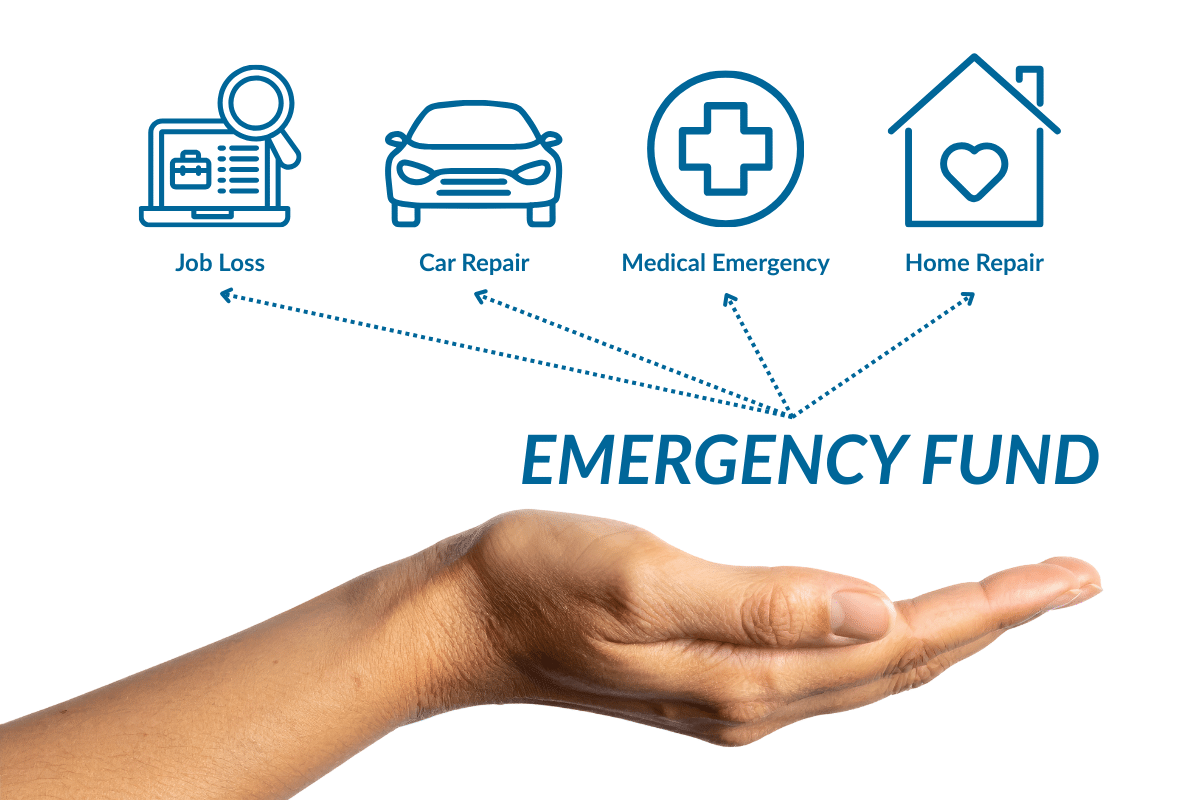

Why Saving Comes Before Paying Off Debt

Q: Should I really put money into savings even though I have a lot of credit card debt?

A: Absolutely. You need an emergency fund… a stash that’s there when life does what it always does and throws you a curveball.

Here’s the reality: if you don’t have cash set aside for emergencies (and trust me, stuff always happens), your only option will be a credit card bailout. That’s how people stay stuck. You can’t get off the credit card debt treadmill if you keep adding new charges, even when the expense is legitimate and unavoidable.

Saving while you’re paying down debt isn’t backward; it’s protective. Set aside something from every paycheck. Ten percent is a solid goal, but if that feels impossible right now, start smaller. The point is to build a buffer so the next emergency doesn’t undo all your progress. That’s how you eventually part company with credit card debt for good.

The Best Way to Choose Which Credit Card to Pay First

Q: Which credit card account should I pay off first? The smallest balance or the highest interest rate?

A: Start with the smallest balance. Here’s why.

We’re emotional creatures, not math robots. We need to see progress sooner rather than later. If the card with the highest interest rate also happens to be your biggest balance, and it often is, you could be staring at that statement for years before seeing real progress. That’s discouraging, and discouragement is what causes people to quit.

But when you knock out a small balance in a few months, something powerful happens. You get to look at a statement that says $0. That quick win delivers an emotional payoff that fuels momentum. And momentum is everything.

Once that first card is gone, you roll what you were paying on it toward the next smallest balance, then the next. One by one, those balances fall until every credit card reads zero. That’s not theory. That’s how people actually succeed.

Where Your Tax Refund Does the Most Good

Q: Should I use my tax refund to pay down credit card debt or stash it into an emergency fund?

A: It depends on how solid your emergency savings are right now.

If you already have enough cash set aside to cover your basic bills for three months without a paycheck because of a job loss, medical issue, or anything else life throws at you, then using your refund to pay down debt is a smart move. That lump-sum payment can reduce balances quickly and save you interest.

But if you don’t have that safety net in place yet, your refund is better spent building one. Think of it as buying yourself breathing room. A healthy emergency fund keeps future surprises from landing back on a credit card and undoing the progress you’re working so hard to make. In that case, parking your refund in savings isn’t cautious… it’s strategic.

When a 0% Balance Transfer Helps and When It Hurts

Q: Should I transfer my debt to a 0% credit card?

A: Maybe. This one’s tricky, and it depends entirely on your situation, the fine print on that shiny new card, and most important, your willingness to use it wisely and not shoot yourself in the foot.

Before you do anything, read the terms. Then read them again. (Good luck. One study found some credit card agreements are written at a 27th-grade reading level.) Look for the landmines: Is there a balance transfer fee? How long does the 0% rate actually last? And what’s the default interest rate if you miss a payment or don’t pay the balance off in time?

For example, transferring a $5,000 balance with a 4% transfer fee costs you $200 right out of the gate. Ouch. And if the teaser rate expires before the balance is gone, that sky-high interest rate can undo your progress fast.

That said, if there’s no transfer fee and you are fully committed to paying the balance off within six months come hell or high water, you might come out ahead. Just don’t confuse a balance transfer with a solution. It’s only a tool, and in the wrong hands, it can make things worse.

Question: If you had to give one piece of debt advice to your younger self, what would it be? Share in the comments below.

More from Everyday Cheapskate

https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should) https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies)

https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies) https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50%

https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50% https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days

https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days https://www.everydaycheapskate.com/wp-content/uploads/20260705-how-to-keep-a-cooler-cold.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:19:502026-07-05 13:19:50How to Pack a Cooler That Stays Cold for 48 Hours

https://www.everydaycheapskate.com/wp-content/uploads/20260705-how-to-keep-a-cooler-cold.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:19:502026-07-05 13:19:50How to Pack a Cooler That Stays Cold for 48 Hours https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom

https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom https://www.everydaycheapskate.com/wp-content/uploads/20260617-how-to-build-a-1000-emergency-fund-jar-with-coins-and-plant.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-17 18:34:002026-06-17 18:34:00How to Build a $1,000 Emergency Fund When Money Is Already Tight

https://www.everydaycheapskate.com/wp-content/uploads/20260617-how-to-build-a-1000-emergency-fund-jar-with-coins-and-plant.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-17 18:34:002026-06-17 18:34:00How to Build a $1,000 Emergency Fund When Money Is Already Tight https://www.everydaycheapskate.com/wp-content/uploads/20260614-how-to-splurge-on-a-budget-woman-drinking-fancy-coffee-luxury-treat-smiling.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-14 20:10:232026-06-14 20:12:40How to Splurge on a Budget Without the Guilt

https://www.everydaycheapskate.com/wp-content/uploads/20260614-how-to-splurge-on-a-budget-woman-drinking-fancy-coffee-luxury-treat-smiling.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-14 20:10:232026-06-14 20:12:40How to Splurge on a Budget Without the Guilt https://www.everydaycheapskate.com/wp-content/uploads/20260607-woman-grocery-shopping-pushing-cart-with-apples-and-cauliflower.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-09 23:20:292026-06-09 23:20:29How to Read a Grocery Store Sale Cycle (And Stop Overpaying)

https://www.everydaycheapskate.com/wp-content/uploads/20260607-woman-grocery-shopping-pushing-cart-with-apples-and-cauliflower.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-09 23:20:292026-06-09 23:20:29How to Read a Grocery Store Sale Cycle (And Stop Overpaying)

You have 2 choices.

1 use an abrasive on the tile. Not a HARSH abrasive mind you. You will probably be surprised at the result. Gently does wonders, even if it does take time…

2 go to a reputable business and ask them. Tell them it’s a small job so not worth their while. Most businesses will be helpful. And if you do need to use them down the track, then do so. And tell them why? They will appreciate the feedback and the business.

Good luck

What is the best way to clean ceramic tile floors? I’m not referring to the grout…just the tiles that I can’t get clean with just water.