5 Smart Reasons Why Kids Should Get an Allowance

Wondering if kids should get an allowance? Giving your child an allowance is more than handing over cash. It’s an opportunity to build financial confidence, encourage responsibility, and raise independent thinkers who understand the value of a dollar. Here’s why it’s one of the best parenting tools you’ll ever use.

Key Points

- Based on years of parenting and thousands of reader stories, a small, steady allowance builds lifelong money skills.

- It’s not about the amount. It’s about helping kids learn to make smart choices, recover from money mistakes, and feel confident managing their own finances.

- For over 30 years at Everyday Cheapskate, we’ve seen how a simple allowance can become one of the most powerful tools for raising financially independent kids.

At the root of financial intelligence lies one undeniable truth: It’s not about how much money you have, it’s about what you do with it. That lesson applies just as much to a child managing a $5-a-week allowance as it does to a high-earning executive juggling thousands. The dollar amount is secondary. It’s the habits and decisions that matter most.

I didn’t always understand that. For years, I believed that more money would solve everything. I clung to the idea that if we could just earn more, win the lottery, or get a surprise inheritance, all our problems would magically disappear. But here’s what actually happened: the more we made, the more chaotic things became. Why? Because we didn’t know how to manage what we already had. We didn’t budget, didn’t save, didn’t give—truthfully, we had no idea where our money was going.

It turns out, more isn’t the solution. It’s financial wisdom that makes the difference, and if our kids don’t learn that early, they’re likely to carry those same destructive patterns into adulthood.

The good news? You don’t need a crash course in economics to help your kids get on the right path. A simple allowance, paired with the freedom to make decisions and experience the consequences, is one of the most powerful tools you can give them. It’s how they’ll learn firsthand about saving, spending, giving, and even regret… all under your roof, with the safety net of your guidance.

Why Giving Kids an Allowance Just Makes Sense

1. Teach Kids About Real Life

Nothing beats an allowance for offering a hands-on course in real-life values. With their own money in hand, kids begin to learn responsibility, delayed gratification, the cost of poor choices, the reward of smart ones, and yes, the importance of giving. It’s a safe way for them to experience real consequences and real wins.

2. Help Distinguish Needs from Wants

Do they really need that new video game? Or those must-have peace sign earrings? When kids are spending their own money, the decision-making shifts. Suddenly, they’re thinking twice and learning to prioritize. And when the money runs out, it runs out. That’s a powerful (and unforgettable) lesson in budgeting.

3. Put an End to the Nickel-and-Diming

An allowance becomes a predictable, line-item expense in your household budget, something you plan for, instead of giving in to every “can I have…” moment. That means you can say goodbye to the constant drip-drip-drip of small purchases and spontaneous spending. It creates structure where there used to be a slow leak.

4. Build Trustworthiness in a Child

Putting money into a child’s hands sends a clear message: I trust you. And with that trust comes responsibility. When kids know they’re being counted on to manage their money wisely, they tend to rise to the occasion. It’s a simple but powerful way to foster maturity, decision-making skills, and accountability.

5. Promote Self-Confidence

There’s something empowering about managing even a small amount of money. Giving kids the tools to save for a goal, give to a cause, and make their own purchasing decisions builds confidence and independence. They begin to see themselves as capable and resourceful, qualities that will serve them well far beyond childhood.

When Should You Start an Allowance?

There are no hard-and-fast rules here, but a good guideline is to wait until your child can understand that money is used to buy things, that stuff costs money, and that choices matter. For most kids, that lightbulb moment happens right around age six. That’s when they’re old enough to grasp the basics: if they spend it all today, they can’t afford the toy next week.

How Much Allowance Should You Give?

Some families use a simple formula, like a dollar per year of age, but that’s just a starting point. A better approach is to look at how much you’re already spending on your child for non-essentials like treats, small toys, or apps. Then, hand over that amount as their allowance instead.

By shifting the control to them, you’re not spending more, you’re simply giving them responsibility for money you would have spent anyway.

Stick to a regular schedule: weekly for younger kids (shorter time frames help them stay focused), and monthly for older kids to encourage budgeting and planning.

Allowance by the Numbers — 2025 Snapshot

A recent Wells Fargo survey offers a revealing look at how families across the U.S. are handling allowances in 2025:

- Average weekly allowance (ages 5–17): $37.19

- Median weekly allowance: $20

- Most common age to start: Ages 9–11, but many families start younger

- Popular formats: 73% of parents still use cash, while others opt for Venmo, direct deposit, or prepaid debit cards

- Only 29% of parents have increased their child’s allowance to match inflation

Whether you give $5 or $25, consistency, structure, and a clear purpose matter more than the exact dollar amount. And don’t worry, digital tools can work with your allowance system, especially for older kids.

Should Allowance Be Tied to Chores?

Here’s where opinions vary, so let’s keep it practical.

If your main goal is to teach money management, keep the allowance separate from household chores. Think of it as a financial training tool, not a paycheck.

That said, if you also want to instill a strong work ethic, you can offer extra money for extra work, like washing the car, cleaning out the garage, or helping with yard work. This hybrid approach teaches both: the value of money and the value of work.

Letting Kids Learn From Their Own Money Mistakes

The whole point of giving an allowance isn’t to control how your kids spend every dime. It’s to teach them how to self-govern. That means allowing them to make choices, even the not-so-great ones.

Encourage them to follow a simple formula: save a set percentage, give a portion to charity (they’ll learn early that giving feels good), and then have the freedom to spend the rest. And yes, sometimes that means they’ll blow it all on bubble gum or another plastic trinket they regret five minutes later.

That’s okay. In fact, that’s the lesson. Better they learn those “oops” moments now, when the stakes are low, than later in life with rent, credit cards, and car payments on the line.

A Hands-On Money Tool That Teaches for Life

If you want to give your kids’ allowance program a strong start, set them up with a simple system for managing their money. A physical tool, like jars, envelopes, or a divided bank, helps them visualize where their money is going and learn the power of planning.

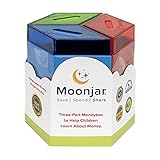

Classic MoonJar Moneybox

One of my favorite tools? The Moonjar Classic Moneybox. It’s a three-in-one savings bank that teaches kids to spend, save, and share, all with their very own money. It’s colorful, sturdy, and intuitive enough for kids as young as four to grasp the concept.

Over the years, Moonjar has won multiple innovation awards, and for good reason. It’s not just a piggy bank. It’s a lifelong teaching tool that helps build habits of generosity, patience, and smart spending.

Real-Life Success from the Hunt Family Plan

On my way to getting a financial life, our kids got one too. Our boys were just 6 and 7 years old when I hit rock bottom, a turning point that changed everything for our family.

Determined that our children wouldn’t grow up to repeat my mistakes, my husband and I created what we called the Hunt Kid Financial Plan. We put it into practice immediately, even though we were buried in debt at the time. Our boys had no idea what was going on behind the scenes, but they took to the plan like ducks to water.

Had it not worked, I wouldn’t have written a book about it. But it did. And I’m proud to say that our sons, now grown, are two uniquely awesome, financially confident men. No credit card debt. No student loans. They each bought their first cars in full, at age 16, with money they saved themselves. Both became homeowners in pricey Orange County, California, by age 25.

We didn’t just turn our finances around, we debt-proofed our kids. And it all started with a simple allowance program.

If you’d like to know more about our journey and the plan that worked for our family, I would be honored for you to read my book, Raising Financially Confident Kids. It’s as relevant and practical today as it was the day we started living it.

Question: What age did you start giving your kids an allowance and did it teach them anything surprising? Let’s compare notes in the comments below.

EverydayCheapskate™ is reader-supported. We participate in the Amazon Services LLC Associates Program and other affiliate advertising programs, designed to provide a means for us to earn from qualifying purchases, at no cost to you.

More from Everyday Cheapskate

https://www.everydaycheapskate.com/wp-content/uploads/20260717-how-to-read-your-water-bill-sprinklers-on-a-residential-lawn.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-18 10:46:312026-07-18 10:46:31How to Read Your Water Bill and Lower Your Monthly Costs Now

https://www.everydaycheapskate.com/wp-content/uploads/20260717-how-to-read-your-water-bill-sprinklers-on-a-residential-lawn.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-18 10:46:312026-07-18 10:46:31How to Read Your Water Bill and Lower Your Monthly Costs Now https://www.everydaycheapskate.com/wp-content/uploads/20260715-high-yield-savings-account-man-dropping-quarter-into-mason-jar.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-15 18:01:312026-07-15 18:01:31The Boring Money Move That Earns You $400 to $2,000 a Year (High-Yield Savings Explained)

https://www.everydaycheapskate.com/wp-content/uploads/20260715-high-yield-savings-account-man-dropping-quarter-into-mason-jar.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-15 18:01:312026-07-15 18:01:31The Boring Money Move That Earns You $400 to $2,000 a Year (High-Yield Savings Explained) https://www.everydaycheapskate.com/wp-content/uploads/20260713-what-to-pack-for-kids-lunchboxes-young-boy-and-girl-eating-a-banana-and-a-sandwich.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-13 21:54:132026-07-13 21:54:13Back-to-School Lunch Ideas for a Week (No Boring Sandwiches)

https://www.everydaycheapskate.com/wp-content/uploads/20260713-what-to-pack-for-kids-lunchboxes-young-boy-and-girl-eating-a-banana-and-a-sandwich.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-13 21:54:132026-07-13 21:54:13Back-to-School Lunch Ideas for a Week (No Boring Sandwiches) https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should) https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies)

https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies) https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50%

https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50% https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days

https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom

https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom https://www.everydaycheapskate.com/wp-content/uploads/20260703-home-decor.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-03 20:46:552026-07-03 20:46:5510 Everyday Items You Never Think to Wash (But Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260703-home-decor.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-03 20:46:552026-07-03 20:46:5510 Everyday Items You Never Think to Wash (But Should)Please keep your comments positive, encouraging, helpful, brief,

and on-topic in keeping with EC Commenting Guidelines

Last update on 2026-07-27 / Affiliate links / Images from Amazon Product Advertising API

I didn’t believe in giving my kids allowance for chores. Chores are a part of a family unit and everyone was expected to help. (I didn’t get paid for being a single mom) I however paid them for good grades. Both of them were in Honors classes. Regular classes, not electives, they got $4/A’s, $3/B’s nothing for C’s or less. In Honor classes, they got an extra dollar. They are now 39 & 40 and I was a single mom to put the numbers in perspective. They did get paid extra for any above and beyond help around the house. They were also on academic grounding if they ever came home with a D or a progress report until it was at least a C. The harder they worked in school, the more they got paid, similar to a job. One of them if financially responsible, the other the opposite, sadly. But she’s turning herself around now at 39.

Teaching finance to children is a lifelong process. Not only does it encompass saving and budgeting, but it also includes teaching the value of purchases as the children age. Using sales, discounts, and coupons are equal parts of saving money. So is determining worth by asking yourself questions – “How badly do I want/need this? Will I use it enough to justify the cost? How does it impact my future need for money? Can I find a better deal by researching online? Is it a good value for the money?” These questions apply to all purchases, large and small. My dad constantly reinforced his mantra: “Protect your name and your credit. Both will travel farther than you ever will. A little money saved gives you more power than having none.”

This is exactly how I was raised back in the 50’s. My first allowance at about 6 was a quarter. I kept 3 jars in my drawer for my 3 different “accounts” – tithe, savings and spending. I was so proud when my mother would come to me for a small loan till she could get to the bank! In Junior High I started getting an annual clothing allowance. We had unpaid chores around the house, because we all shared the resources and the responsibilities. I also cleaned my grandmother’s studio apartment weekly for extra cash. I am so grateful for the lessons taught to me by my parents about financial responsibility.

Oh, Mary, how wonderfully right you are! I got an allowance as a child, and had great input from my parents about money management growing up. So my kids got a small one as well. But it wasn’t until one day in Target during a clothes shopping trip that we turned a corner. My oldest was in 7th grade, and up until then, we had seen eye-to-eye; but on that day, she suddenly disliked every outfit I recommended. I didn’t respond very well, and in frustration, handed her the envelope containing the cash I had earmarked for her clothing money. I told her, “This is what I have budgeted. You spend it as you please, but when it’s gone, there won’t be any more until next month.” Right before my eyes, she became a frugal shopper, and headed to the clearance rack! Because it was now her money, she wanted it to go as far as possible. Not only that, she also began to ask for help, and I became her ally. It wasn’t long before I instituted a larger monthly allowance to cover other things as well—things I was already paying for, like lunch money, gifts for her friends’ birthdays. She felt rich, and handled it beautifully. I think it taught me as much as it taught her, and each of my children, in turn, looked forward to this rite-of-passage.

I wish I’d kept track of every response/feedback like yours I have received over the years. Thanks for sharing!

We got a $1 per age for allowance growing up. Now I give my kids $3 per age once a month. They need to learn how to spend and save money. My 16 year old daughter has 50,000 sitting in a bank account for an auto accident and has money put aside for college (from her grandparents) and still adds to her bank account once a month. She also makes money babysitting, dog walking and making jewelry. I am so proud of her.

I think children are entitled to a part of the family income as is everyone else. The amount of course has to be considered in terms of age and needs. My kids got an allowance from age 7 – if I remember it was $1 a week. I wasn’t so well versed in financial matters that I thought of the save/spend ratio but it was theirs’s to do with as they pleased. The amount went up $1 each year and when they were 12 I gave them $20 but included their clothing spending in it. They always had money in their pockets.