Thinking of Lending Money to Family or Friends? Read This

It usually starts with a simple ask. Someone you care about needs help, and your first instinct is to say yes. After all, it’s family… or a close friend… not a stranger off the street. But here’s the part no one likes to talk about: lending money to family can quietly change relationships. Over the years, I’ve heard from readers who meant well but ended up frustrated, resentful, and out a chunk of cash they couldn’t easily replace. The good news? A little planning upfront can protect both your wallet and your relationship and save you from a whole lot of stress later.

Over the years, I’ve heard from dozens of readers who lent money to friends or family only to feel blindsided when things didn’t go as planned. Some were small $50 loans and others were $28,000 family loans!

The pattern is almost always the same: they reach out after the loan has gone sideways, sometimes months, even years later, hoping for a solution to get their money back.

I wish they had written before handing over the money. Because doing this right from the beginning changes everything.

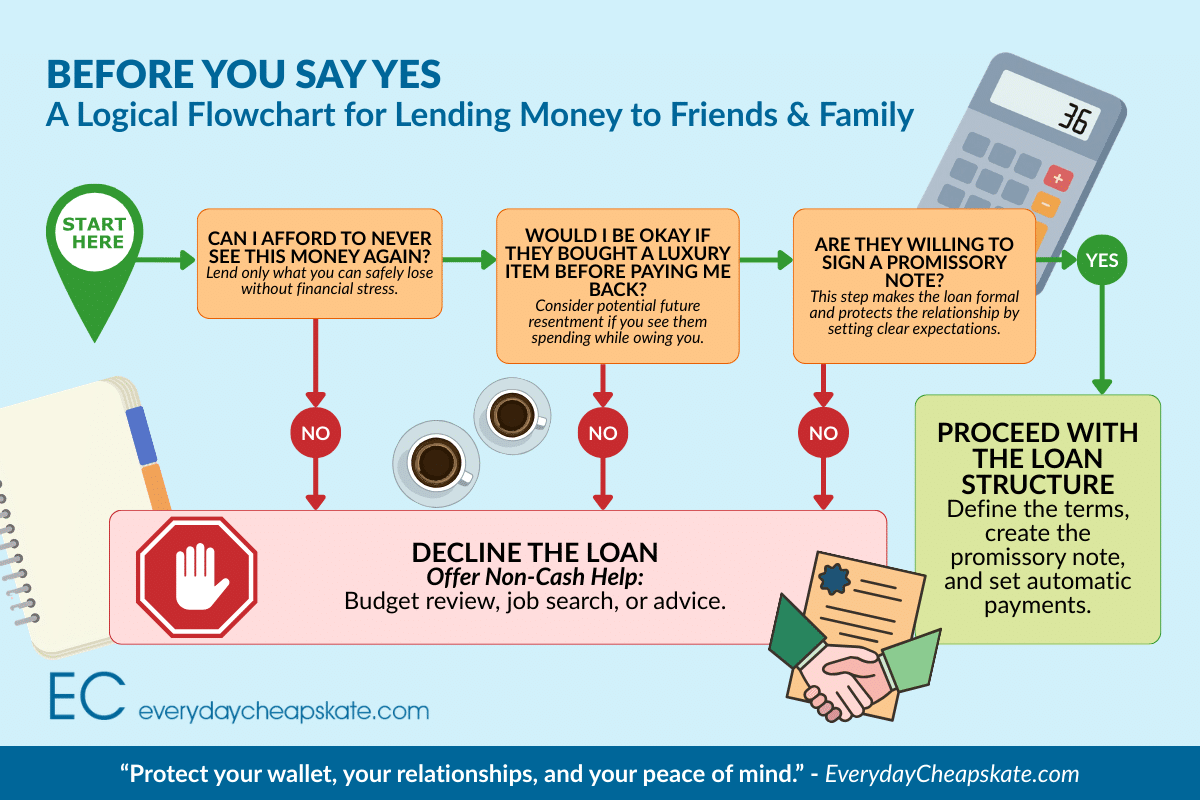

Accept Reality (Even If It’s Uncomfortable)

Lend only what you can afford to give as a gift. Don’t say that out loud, but be honest with yourself.

There’s a reason your borrower is coming to you instead of a bank or credit card. That doesn’t make them a bad person. It just means there’s risk involved.

If repayment doesn’t happen, will you still be okay financially and emotionally? If the answer is no, it’s better to pause right here.

Set Expectations Early (This Changes Everything)

I know it feels uncomfortable to talk details when you’re trying to help someone you care about. So most people skip it. They keep things casual, trusting it will all work out. And that’s usually where things start to unravel.

A quick, honest conversation upfront can save you months of frustration later. Talk through the basics before any money changes hands:

- How much is being borrowed?

- When and how it will be repaid?

- What happens if something unexpected comes up?

This isn’t about making things awkward. It’s about making things clear. Because once expectations are out in the open, you’re not guessing… and you’re not chasing anyone down later. That’s a whole lot easier on both of you.

Put It in Writing: Promissory Note

This is where things shift from “we’ll figure it out” to “we both know the plan.”

A promissory note is simply a written agreement that spells everything out:

- Total amount

- Payment schedule

- Due dates

- Consequences if payments are missed

It might feel a little formal, especially if you’re dealing with someone close. But in my experience, this step actually protects the relationship. Why? Because no one has to rely on memory, assumptions, or “I thought you meant…”

You can easily find free templates online (search “free promissory note”) and fill in the blanks in minutes. It sets the tone that this is a real commitment… not a vague promise.

Charge a Reasonable Interest Rate

Charging interest can feel a little awkward at first. I get it. But it actually helps set the tone that this is a real loan, not just a casual favor that can slide indefinitely. It also keeps things fair for both of you.

And here’s something most people don’t realize: the IRS expects lenders to charge at least a minimum interest rate (called the Applicable Federal Rate), and that number changes over time.

Even a modest rate keeps things fair and avoids confusion down the road.

Require Collateral (When It Makes Sense)

If you’re lending a larger amount, it’s reasonable to ask for a little backup plan. That’s where collateral comes in.

This simply means the borrower offers something of value (i.e., electronics, tools, jewelry, even a collectible) as a way to secure the loan.

And here’s the important part: take possession of it. Be sure to spell it out in your written agreement:

- What the item is and its condition

- That it’s returned once the loan is paid in full

- That it becomes yours if the loan isn’t repaid

It may feel a bit formal in the moment, but it’s one of the simplest ways to keep things clear and avoid hard feelings later.

Create a Repayment Plan That Actually Works

Good intentions don’t make payments. Systems do. Before any money changes hands, agree on a plan. Do it while everyone is still feeling positive and committed to making this work.

And here’s a tip that will save you a lot of frustration later: let the borrower suggest the plan. You can always adjust it together, but it gives you a realistic starting point.

Better yet, make it automatic. Automatic transfers remove the guesswork, the reminders, and the awkward “Hey, just checking in…” call. It keeps things predictable and preserves the relationship.

There’s an App for That (And It Helps)

Of course there’s an app for this, because of course there is. But in this case, it can genuinely make things easier.

Apps like Zirtue are designed specifically for lending money between friends and family without all the guesswork and awkward follow-ups.

Here’s what I like about it:

- You can set clear terms from the start

- Payments are automatic (no chasing required)

- Everything is tracked in one place

One newer feature that stands out is the option to send money directly to a biller like a utility or phone company. That means you know exactly where the money is going, which can bring a lot of peace of mind.

It also builds in structure:

- No credit checks

- Set repayment schedules

- Optional protections like payment coverage in certain situations

Now, to keep this real, no system is perfect. The borrower may pay a small fee, and like anything involving money, it still depends on both people following through. But if you’re looking for a way to keep things organized, reduce tension, and avoid awkward conversations, this is a solid option to consider.

Sometimes a little structure is exactly what keeps a good relationship from getting strained.

When It’s Better to Say No

This may be the hardest part of all. Sometimes, the best thing you can do for both of you is say no.

If lending the money is going to stretch your budget, keep you up at night, or create tension in your own home, that’s a sign to pause. Not every request is a good fit, no matter how much you care about the person asking.

And saying no doesn’t mean you’re turning your back on them. You can still offer help in other ways:

- Sit down and help them look at their numbers

- Talk through possible options

- Or give a smaller amount that you’re comfortable treating as a gift

Lending money to someone you care about isn’t just a financial decision. It’s a relationship decision. Handled well, it can strengthen trust. Handled casually, it can quietly damage even the closest connections. And protecting your peace doesn’t make you selfish. It makes you wise.

A little structure upfront may feel formal in the moment but it’s what keeps things respectful, clear, and drama-free in the long run.

Question: Have you ever lent money to family or a friend and would you do it the same way again? Share in the comments below.

More from Everyday Cheapskate

https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days

https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom

https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom https://www.everydaycheapskate.com/wp-content/uploads/20260703-home-decor.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-03 20:46:552026-07-03 20:46:5510 Everyday Items You Never Think to Wash (But Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260703-home-decor.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-03 20:46:552026-07-03 20:46:5510 Everyday Items You Never Think to Wash (But Should) https://www.everydaycheapskate.com/wp-content/uploads/20260630-a-lit-sparkler-with-an-american-flag-in-the-background-4th-of-july-hacks-tips-and-recipes.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-30 21:44:502026-06-30 21:44:5034 Fourth of July Recipes and DIY Hacks for a Stress-Free Holiday

https://www.everydaycheapskate.com/wp-content/uploads/20260630-a-lit-sparkler-with-an-american-flag-in-the-background-4th-of-july-hacks-tips-and-recipes.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-30 21:44:502026-06-30 21:44:5034 Fourth of July Recipes and DIY Hacks for a Stress-Free Holiday https://www.everydaycheapskate.com/wp-content/uploads/20260629-wooden-die-spell-july-with-patriotic-decor-in-background.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-29 21:07:092026-06-29 21:10:297 Best Things to Buy in July for Huge Summer Savings

https://www.everydaycheapskate.com/wp-content/uploads/20260629-wooden-die-spell-july-with-patriotic-decor-in-background.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-29 21:07:092026-06-29 21:10:297 Best Things to Buy in July for Huge Summer Savings https://www.everydaycheapskate.com/wp-content/uploads/20260628-Grilled-Peaches-with-Balsamic-and-Blue-Cheese-1.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-29 09:38:342026-06-29 09:38:34Summer Grilled Peaches with Balsamic and Blue Cheese

https://www.everydaycheapskate.com/wp-content/uploads/20260628-Grilled-Peaches-with-Balsamic-and-Blue-Cheese-1.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-29 09:38:342026-06-29 09:38:34Summer Grilled Peaches with Balsamic and Blue Cheese https://www.everydaycheapskate.com/wp-content/uploads/20260625-a-rustic-wooden-christmas-tree-in-the-sand-on-the-beach.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-26 11:34:132026-06-26 11:36:44Christmas in June? Try This Amazon Prime Day Gift Guide

https://www.everydaycheapskate.com/wp-content/uploads/20260625-a-rustic-wooden-christmas-tree-in-the-sand-on-the-beach.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-26 11:34:132026-06-26 11:36:44Christmas in June? Try This Amazon Prime Day Gift Guide https://www.everydaycheapskate.com/wp-content/uploads/20260624-why-does-my-ice-taste-weird-soda-tea-lemonade-juice.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-24 17:10:532026-06-24 17:10:53Why Does My Ice Taste Weird? Here’s the Answer

https://www.everydaycheapskate.com/wp-content/uploads/20260624-why-does-my-ice-taste-weird-soda-tea-lemonade-juice.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-24 17:10:532026-06-24 17:10:53Why Does My Ice Taste Weird? Here’s the Answer https://www.everydaycheapskate.com/wp-content/uploads/20260622-a-single-car-garaged-with-beautiful-flowers-along-landscape-beds-things-ruined-by-heat-in-the-garage.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-22 20:24:432026-06-22 20:24:4325 Things Summer Heat Can Ruin in Your Garage

https://www.everydaycheapskate.com/wp-content/uploads/20260622-a-single-car-garaged-with-beautiful-flowers-along-landscape-beds-things-ruined-by-heat-in-the-garage.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-22 20:24:432026-06-22 20:24:4325 Things Summer Heat Can Ruin in Your Garage

in reading this, i saw a lot about promissory notes but not a word about getting it notarized. i lent a friend money and when i wasn’t paid back i tried to take legal action but was told without the signature and seal of a notary a promissory note means squat.

That’s technically not the case. Even a verbal agreement is enforceable by law. The issue arrises when you have to prove it. So yes, anything that will help you prove the agreement will only help.

Suze Orman says to never loan money unless it’s to fix a temporary problem. If you loan money to someone who’s always broke, you’re just delaying the inevitable crash. I wish I’d heard that years earlier before I loaned a relative money. She worked hard, but she was married to a bum who wouldn’t work. They were always short money. I only received a few payments (about 25% of what she owed me). Several years later, she was destitute again, and I gifted her $2000. She was very grateful. I made up my mind that that would be the last time. She never asked me for more, but she was broke until the day she died. After her death, I learned that she’d gotten heavily into payday loans.

I’ve been allowing my adult children to use my credit card. 0% balance transfer offers. Two have always repaid me in full, including the fees the credit card company charges. One is rarely able to make a payment. When I die, it’ll all come out of his small inheritance.

I learned years ago it is easier to just gift the money and not look for something that isn’t coming. The person you loan the money to has no intention of paying it back and every time you see them they say, “I haven’t forgotten I owe you money.” That is a clear sign they are trying to clear their conscience about the debt.

We loaned money twice to family members without any contract. One paid $25 twice on a $2000 loan. The other was to receive a large divorce settlement so we loaned $28,000. She started doing drugs which totally derailed the large settlement. We have received $400 and probably will not receive much more. This has caused deep hard feelings. They both have had the nerve to come back and ask for more. We declined.

Another time I loaned $1,000 to an 18yr old son of a friend. I agreed to this knowing it might not work and willing to forgive the loan if needed. We set up a free student checking account for him at my bank which enabled him to easily send me money, set a low weekly payment amount and he repaid $800 as agreed. I forgave the final $200 as a gift because I was so proud of him.

I personally borrowed $5,000 that was offered from a friend many years ago. There was a definite re-payment plan with low interest. I never missed a payment.

Loans to friends and family can work and be helpful but I would advise anyone considering loaning money to seriously take Mary’s advice.

I “loaned” my niece a great deal of money. She and husband were “desperate” have three children. Husband had lost his job. Crying, Begging. Immediate need. All kinds of promises to pay back as soon as possible. Months go by. I reminded. Long story. I wound up having to put aside the loan to “save the Family” Never got a cent back, or even a thank you.

I really appreciate Everyday Cheapskate. I often wonder where you get your bright ideas.

I have loaned money but with the attitude that if I never saw the money again it wouldn’t destroy our friendship. I loaned money last year to a friend that had the plan all laid out how and when he was going to pay it back. Instead of getting total payment in July as promised, I finally got the final payment 2 weeks ago with more than fair interest. I wasn’t the least bit concerned about him paying it back. I was just concerned that if anything at all had happened to him, I had no collateral at all so I’d have been out of luck. Therefore, I’ve decided that there will be no more loans.

There have been a couple financial crisis among family but I have just given money rather than a loan. It’s so much easier on the nerves and relationships.

If I can afford to, not very often, if friends, or family ask me for a loan, I tell them it’s a Gift. And to “pay it forward”. Do a kindness for someone, give of Themselves!! Usually I know in advance they Will Not be Able to pay it back in cash. My cousin was fired from her job, just before Christmas. She has two beautiful daughters and no savings. My Gift brought them Christmas and I get prayers every night.

Alright Mary, I love your column, and I’ve used your advice on products and recipes for many years! But this time you’ve missed the boat. In the past, I have lent money to friends, and rarely has it turned out well. Remember, the borrower is servant to the lender? So now I absolutely refuse to loan money to anyone. Friend, family, neighbor, doesn’t matter. Now there have been several instances where I have been approached by people asking for a loan. Again, I never give them a loan. However, there have been many circumstances where someone is doing the right thing, and making the right decisions, and they just need some help. In these cases, I will GIVE them the money and tell them to pass it on to someone else someday who is having a hard time. Then I stress that I do not want the money repaid back to me. This has worked perfectly. And based on what I’ve seen through other people and friends, has saved me lots of headaches and grief.

Jeff,

I think Mary would agree with you about not lending money. Remember, she starts with the advice to not lend more than you are willing to give as a gift. BUT she knows quite well that people are going to do this anyway, so she is doing her best to help us do it wisely.

I live in a culture where people borrow money all the time, and wish someone had told me from the get-go what you have learned — better to give a gift than lose a friend! Even if what I give is much less than the loan they requested, the fact that it comes with no strings attached cements rather than destroys the relationship.

I took a course called Financial Peace University lead by Dave Ramsey. He stated in the class video that when you decide to loan to anyone do so with a mindset that it is a gift and don’t expect repayment. Think about how it may affect your relationship with that person. Then our son asked for us to co sign the loan on his house. We just told him that we worked hard for our credit rating and his credit rating was not good because he was not as good at managing money. We explain es we could not carry their more if they defaulted on the loan and could not co sign. Since that time he has cleaned up his credit score and is very proud how he did it and got a house loan on his own merit. I firmly believe we have to teach our children to stand on their own financially. We will not always be there to fix it for them.

Yes, things were always tight while raising our kids, but I’m now in a position to be able to help them when they need it. It’s a great feeling and they have never reneged on a loan. I always have them sign a promissory note, and I charge them 5% interest. They receive a spreadsheet with monthly payment clearly outlined. I’ve also helped a sister and a nephew, with same loan plan. Everyone knows that, should I die, any unpaid balance becomes part of the estate, and still needs to be repaid, or deducted from their share of any inheritance. I have friends who are appalled that I Expect repayment from family and that I charge my kids interest But, my kids understand that this money is a blessing and that I need this to be comfortable for however long I live I’m hoping for at least another good 20 years-and they are hoping I spend it all! Best kids ever!

I think the most important point is #1 – Accept Reality. I let money to my nephew who was in a bad way at the time, about to be homeless, contingent on a payout he was going to get from an estate (I knew this to be true.) The payout came, and I’ve not gotten anything. I went into this knowing I was doing a good thing, but also knowing the likelihood was 99% I would not get it back.

Certainly I did what I could, but I’m not stressed over it because I already considered it a “gift” (would not get it back) so no stress about it.

Yes, we have lent money multiple times including to parents, siblings, and friends with good results. They paid back as promised. There were two occasions where we were not repaid. The first was 35 years ago. I had to take a break from working on my masters degree when we weren’t repaid. The second was to a nephew who to date has made only minimal payments. Knew there was a chance he wouldn’t repay but wanted to support his son going to science camp. I will not lend to him again

Don’t lend money to your friend if you value the friendship. Something shifts when they take the money from you. We loaned over $3,000 to longtime friends. When they made no move to pay it back, we just had to accept that we’d lost the money and the relationship. It went further south when they called a year later and asked to borrow another $1,000. This was years ago but it still stings.

My brother suddenly took an early retirement so he could move in with our mother to care for her. I lent him $1000 since it was too early for him to collect social security.

I lent it to him knowing that he may not be able to ever repay me but also knowing he was there caring for our mom.

About 2 months ago, I received a check from him for $1100 (I made him take back the extra $100 he included for interest). He was able to pay me once he got his first SS check.

That is a good brother you have there!

I like the way a certain TV judge gives money to people. Let’s say the person wants $500. she will tell them “I’ll give you $250. as a gift, you don’t have to me back” but don’t ask me for money again. It’s fair to say you won’t see that person again at least for borrowing money.