5 Simple Money Habits That Change Everything

Tired of feeling like your money manages you instead of the other way around? Let’s flip the script. By focusing on a few key habits, you can spark a chain reaction that touches every part of your life. These aren’t big, intimidating shifts. They’re simple, manageable steps that make financial peace feel possible.

Ever notice how one small change can ripple through your life like a line of dominoes? That’s the magic of a keystone habit. While a regular habit might nudge your routine in one direction, a keystone habit can reshape the way you think, act, and even feel. In other words, it doesn’t just improve one part of your life. It sets off a cascade of improvements across the board.

Keystone habits are simple and manageable, yet their impact is anything but small. Once in place, these habits build momentum, boosting confidence, reducing stress, and helping you make smarter financial choices naturally.

Habits form when cues trigger behaviors that deliver a reward. Keystone habits go a step further. They create a chain reaction. Take automated savings: transferring money into a separate account each month often sparks smarter spending, better budgeting, and even improved long-term goal planning. That’s the domino effect in action.

The key is to start small and stay consistent. Focus on recognizing the habits or patterns that hold you back, and replace them with simple, manageable routines that support your goals. Unlike relying on willpower alone, keystone habits build momentum over time, gradually shaping both your behavior and your approach to money, making financial peace feel achievable rather than overwhelming.

Nail a few of these, and suddenly budgeting, saving, and planning for the future feel less like chores and more like second nature.

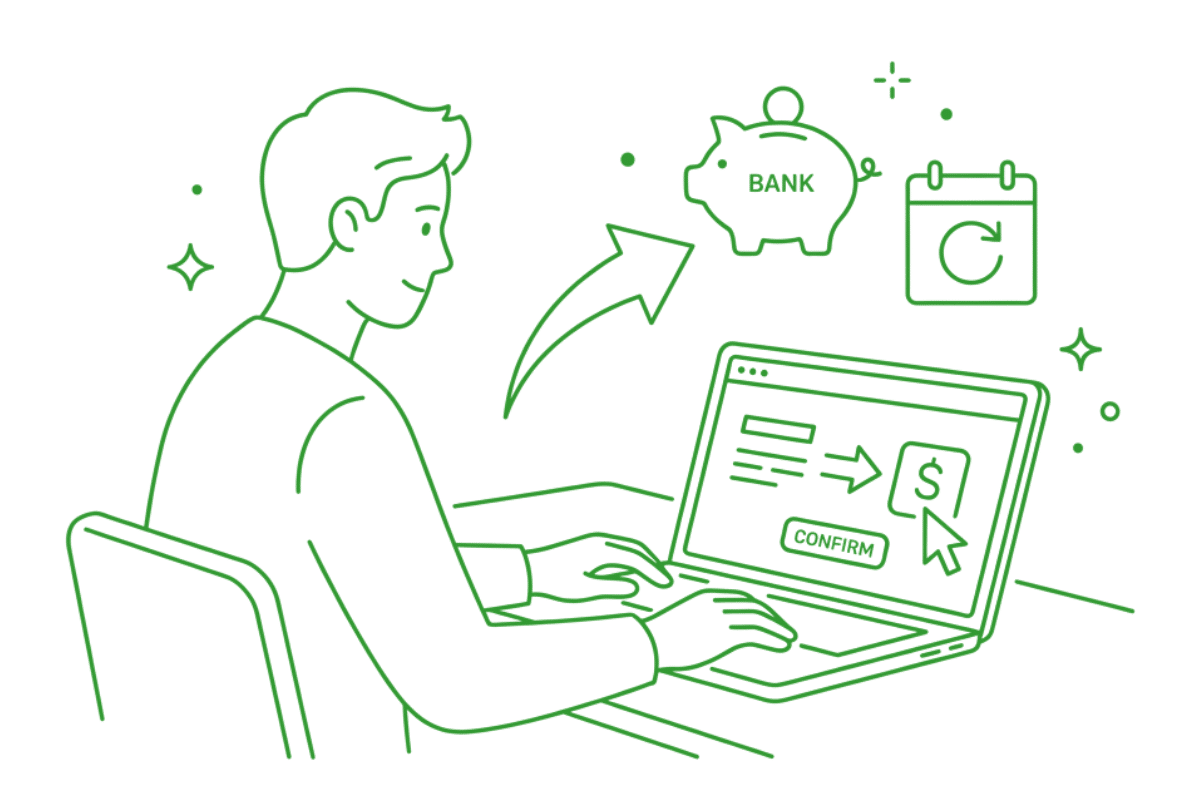

Habit 1: Automate Your Savings and Payments

One of the simplest yet most powerful keystone habits for your finances is automation. Setting up automatic transfers to savings accounts, retirement funds, or investment accounts ensures you’re paying yourself first without having to think about it. The same goes for recurring bills: automatic payments help you avoid late fees, protect your credit, and free up mental bandwidth for other decisions.

Automation isn’t just about convenience. It creates a ripple effect. Once you see your savings grow consistently, you’re more likely to make smarter spending choices. You might skip that impulse buy or rethink a subscription because your money is already working toward your goals. Over time, this habit builds confidence, reduces financial stress, and reinforces the sense that you’re in control of your money… not the other way around.

Start small: pick one account to automate, or set up autopay for one recurring bill. Once you see the benefits, expand to others. The key is consistency. Over time, automation transforms money management from a chore into a natural, effortless part of your routine.

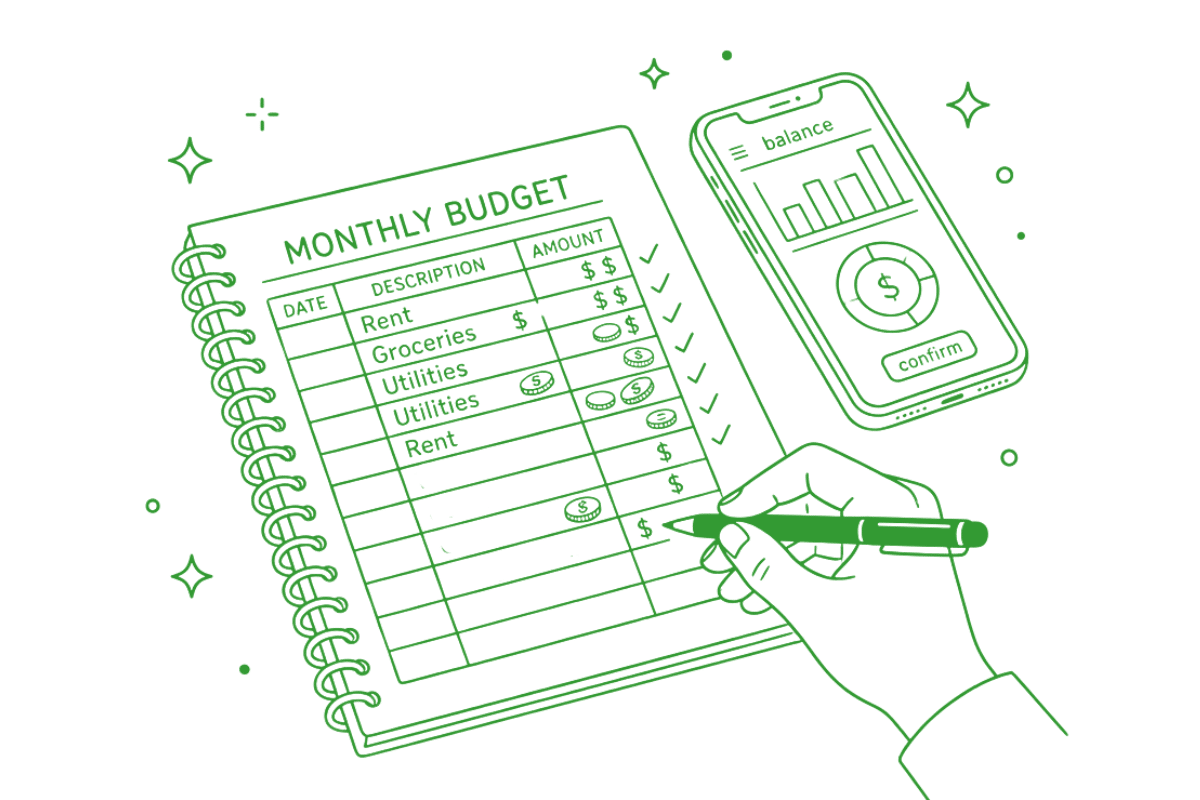

Habit 2: Track Every Dollar You Spend

Knowing where your money goes is the first step toward taking control. Tracking every dollar (yes, every single one!) turns vague spending habits into clear, actionable insights.

I started by tracking groceries with cash only… no plastic allowed. Every dollar I spent had a name and a purpose. That simple habit didn’t just curb spending; it trained me to notice patterns.

This habit doesn’t have to be complicated. Whether you prefer a simple notebook, a spreadsheet, or a budgeting app, the key is consistency. Make it part of your routine, daily or weekly, and watch how it shifts your relationship with money.

The magic of tracking is in the ripple effect. Once you’re paying attention, you start questioning impulsive purchases, spotting subscription creep, and thinking twice before overspending.

Start with one week of tracking, then build from there. Over time, this habit becomes a keystone in your financial foundation, giving you insight, confidence, and a clear picture of your money at all times.

Habit 3: Plan Your Purchases with Purpose

Impulse buying is sneaky. It slips in when we’re tired, stressed, or scrolling online. Planning your purchases with intention flips the script. Instead of reacting to every sale or sudden urge, you decide what truly adds value to your life and what doesn’t.

Before I planned purchases, I’d scroll and click without thinking. Once I started giving myself a 24-hour pause on bigger buys, I realized many ‘must-haves’ weren’t so essential after all. Planning my purchases helped me feel in control instead of reactive.

Start by creating a simple framework: list your needs, set priorities, and give yourself a cooling-off period before big purchases. Even a 24-hour pause can prevent regretful spending. For recurring expenses, consider batching purchases or setting a monthly allowance for non-essentials.

This habit has a domino effect. When you buy with purpose, you automatically reduce clutter, save more, and focus your resources on experiences and goals that matter most. Over time, thoughtful purchasing becomes second nature, turning conscious choices into a financial rhythm that supports your bigger picture.

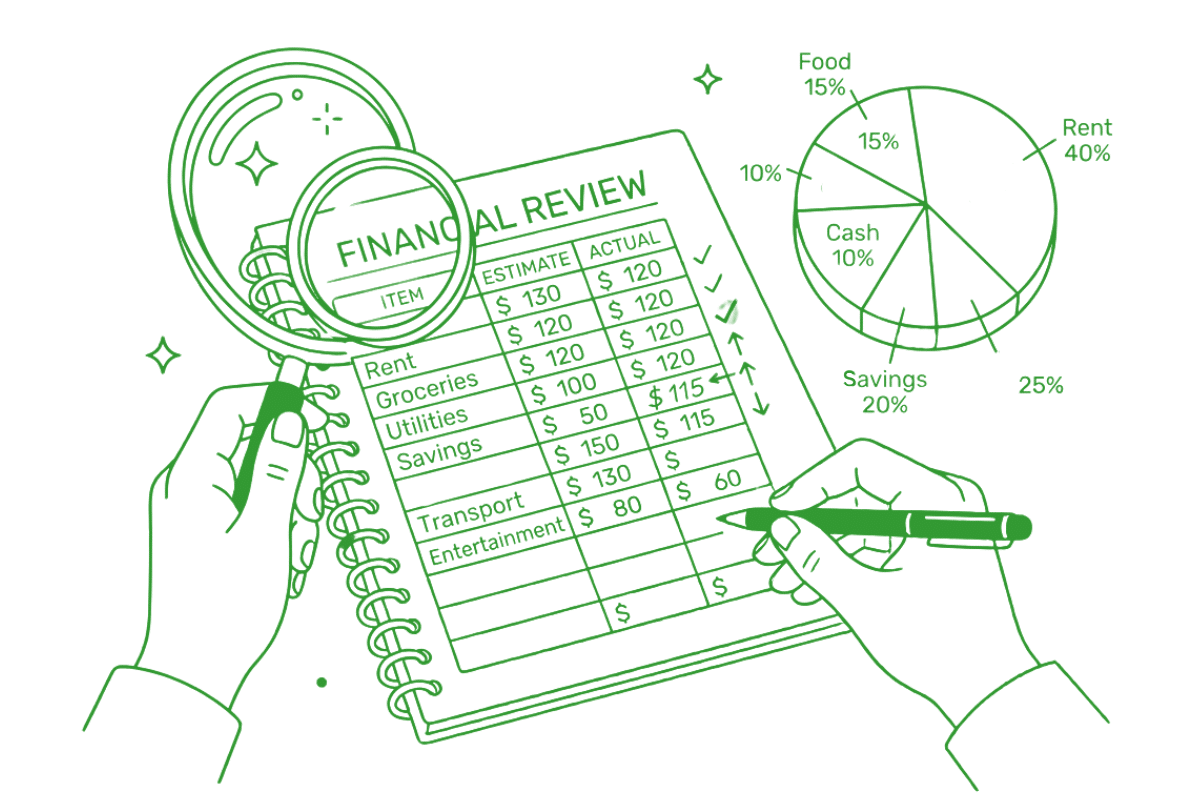

Habit 4: Review and Adjust Your Budget Regularly

A budget isn’t set-it-and-forget-it. It’s a living document that grows with your life. Reviewing your budget regularly keeps you in control and prevents small oversights from snowballing into stress.

Set a recurring monthly, or even weekly, check-in to track your income, expenses, and progress toward your goals. Look for patterns: Are certain categories creeping up? Are there subscriptions or habits quietly draining your account? Use these insights to adjust your spending and make smarter choices going forward.

This habit doesn’t just improve your finances. It changes your mindset. Regular reviews turn money management from a chore into a clear, empowering process. Over time, you’ll find that staying on top of your budget boosts confidence, reduces anxiety, and makes planning for future goals feel achievable, not overwhelming.

Habit 5: Celebrate Small Wins to Stay Motivated

Progress, even small, deserves recognition. Celebrating wins keeps your momentum going and reminds you that your efforts are paying off. It could be as simple as treating yourself to a favorite coffee after hitting a savings milestone, enjoying a guilt-free night out after sticking to your budget, or even just marking a calendar with a happy checkmark.

Even little wins, like having cash left in my grocery envelope at the end of the week, felt huge. Those celebrations kept me motivated and reminded me that progress, however small, matters.

Acknowledging your achievements reinforces the habits you’re building, making it easier to stick with them over time. Without celebration, even positive changes can feel like chores, but a little recognition turns consistency into something satisfying.

These moments of celebration don’t have to break the bank. They’re about mindset, not money spent. By taking the time to notice progress, you’re training yourself to value your discipline, creating a cycle of motivation that keeps your financial habits strong and your confidence high.

How These Money Habits Trigger a Positive Domino Effect

When you put these habits into practice, something powerful happens: one positive change sparks another.

I didn’t go from debt to financial confidence overnight. It was one small habit at a time: cash-only groceries, automated savings, tracking every dollar, and celebrating wins. Each domino fell in sequence, building momentum until managing money felt natural.

The same chain reaction is possible for you. Start small, stay consistent, and watch your habits transform your financial life.

Question: What’s one tiny money habit you’ve started that ended up making a bigger impact than you expected? Share in the comments below.

More from Everyday Cheapskate

https://www.everydaycheapskate.com/wp-content/uploads/20260715-high-yield-savings-account-man-dropping-quarter-into-mason-jar.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-15 18:01:312026-07-15 18:01:31The Boring Money Move That Earns You $400 to $2,000 a Year (High-Yield Savings Explained)

https://www.everydaycheapskate.com/wp-content/uploads/20260715-high-yield-savings-account-man-dropping-quarter-into-mason-jar.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-15 18:01:312026-07-15 18:01:31The Boring Money Move That Earns You $400 to $2,000 a Year (High-Yield Savings Explained) https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should) https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies)

https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies) https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50%

https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50% https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days

https://www.everydaycheapskate.com/wp-content/uploads/20260705-Best-Coolers-for-Camping-Road-Trips-and-Beach-Days.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:26:172026-07-05 13:26:17Best Coolers for Camping, Road Trips, and Beach Days https://www.everydaycheapskate.com/wp-content/uploads/20260705-how-to-keep-a-cooler-cold.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:19:502026-07-05 13:19:50How to Pack a Cooler That Stays Cold for 48 Hours

https://www.everydaycheapskate.com/wp-content/uploads/20260705-how-to-keep-a-cooler-cold.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-05 13:19:502026-07-05 13:19:50How to Pack a Cooler That Stays Cold for 48 Hours https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom

https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom https://www.everydaycheapskate.com/wp-content/uploads/20260617-how-to-build-a-1000-emergency-fund-jar-with-coins-and-plant.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-17 18:34:002026-06-17 18:34:00How to Build a $1,000 Emergency Fund When Money Is Already Tight

https://www.everydaycheapskate.com/wp-content/uploads/20260617-how-to-build-a-1000-emergency-fund-jar-with-coins-and-plant.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-17 18:34:002026-06-17 18:34:00How to Build a $1,000 Emergency Fund When Money Is Already Tight https://www.everydaycheapskate.com/wp-content/uploads/20260614-how-to-splurge-on-a-budget-woman-drinking-fancy-coffee-luxury-treat-smiling.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-14 20:10:232026-06-14 20:12:40How to Splurge on a Budget Without the Guilt

https://www.everydaycheapskate.com/wp-content/uploads/20260614-how-to-splurge-on-a-budget-woman-drinking-fancy-coffee-luxury-treat-smiling.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-14 20:10:232026-06-14 20:12:40How to Splurge on a Budget Without the Guilt

Hi Mary! I love your column so much. Big fan for many years!

OK…money saving tip:

My husband likes Land of Lakes soft butter with canola oil. It is upwards of 8.99 for the large size plastic container. He uses one or more a week.

I discovered I can make my own and its delicious at a fraction of the price:

1 stick of butter (4 oz)

4 oz. Oil (i use a mix or canola and olive oil)

4 oz. Water.

In a Ninja or other food processor, blend butter and oil for 30 seconds.

When blended, add 4 oz of water.

Keep blending, pulsing, whipping…whatever your machine does about a minute.

Pour into a container. I use glass with lid. Refrigerate about an hour and you have spreadable butter.

I get butter on sale fir 2.99 a pound. That is .75 cents per stick. 4 oz of oil is about the same or less. Water is free.

Net savings 7.00 per container.

Also, water has no calories and oil has no saturated fats.

Thats about 30.00 a month, around 350 a year!

Hi Mary! I love ypur column so much. Big fan for many years!

OK…money saving tip:

My husband likes Land of Lakes soft butter with canola oil. It us uowards of 8.99 for tge large size plastic container. He uses one or more a week.

I discovered I can make my own and irs delicious at a fraction of the price:

1 stick of butter (4 oz)

4 oz. Oil (i use a mix or canola and olive oil)

4 oz. Water.

In a Ninja or other food processor, blend butter and oil for 30 seconds.

When blended, add 4 oz of water.

Keep blending, pulsing, whipping…whatever your machine does about a minute.

Pour into a container. I use glass with lid. Refrigerate about an hour and you have spreadable butter.

I get butter on sale fir 2.99 a pound. That is .75 cents per stick. 4 oz of oil us about the same or less. Water is free.

Net savings 7.00 per container.

Also, water has no calories and oil has no saturated fats. Thats a B put 30.00 a month, around 350 a year!

back when toll bridges took cash payments, i’d put all my coins in an empty fish oil bottle and kept it in a cup holder in my car. a local convenience store was experiencing a severe coin shortage. wanting to be helpful, i went in with my bottle of coins. there was more than $50 in that small bottle! i still put all my change in that bottle and from time to time i empty it out, wrap it and deposit it.

These are great workable techniques!!!

Thank you so much Mary!!

We have a younger co-worker who was “lamenting” the cost of a new furnace/AC/refrigerator…not now but in the future. Another coworker and I (we are both 50-60’s) told her to open a credit union savings/checking account and put a little money away automatically out of her paycheck each time. The other day she proudly told me that had saved $1000 already! I told her how proud I was of her, and now she calls it her “emergency animal fund”…..so much for a furnace! 🙂

Since I retired, I have transferred what ever money is leftover each month to savings when my next social security check is deposited. I also transfer the amount saved on the receipt when purchasing groceries or other items to savings. Then if there is an unexpected expense, I am ready for it.