The Boring Money Move That Earns You $400 to $2,000 a Year (High-Yield Savings Explained)

Let’s talk about the least exciting way to make money I know. No stock picks. No side hustle. No 5 a.m. anything. You just move money you already have from one account to a slightly better one. That’s it. That’s the whole trick. And most people never do it.

If your emergency fund and general savings are sitting in a checking or savings account at your regular big bank, there’s a very good chance you’re earning somewhere between 0.01 and 0.50 percent interest on that money. Meanwhile, online-only banks and a handful of higher-yield brick-and-mortar options are currently paying between 3.50 and 4.20 percent on the exact same kind of account. Same FDIC insurance. Same easy access to your cash. Just a much better rate.

That difference, on money you’re already keeping around for emergencies and planned expenses, comes out to $400 to $2,000 a year for a lot of households. For doing nothing but switching where it sits.

Why Your Bank Pays You Peanuts

Here’s the part nobody explains at the branch. Your big bank doesn’t need to compete for your savings. They already have your checking account, your debit card, your loan, and your undivided attention. Why pay up for money that isn’t going anywhere?

Online banks don’t have that luxury. They have to earn your deposits, so they pay for them. That’s the entire story behind that rate gap, and it’s been true for years.

What a High-Yield Savings Account Actually Is

A high-yield savings account (HYSA) is a regular FDIC-insured savings account, just like the one at your local bank, with one meaningful difference: the interest rate is much higher.

Key features of a good HYSA:

- FDIC-insured up to $250,000 per depositor, per bank (same as any bank)

- No monthly fees at any account tier you’d actually use

- No minimum balance requirement at the good ones

- Easy transfers to and from your regular checking account (usually 1 to 3 business days)

- No lockup. You can withdraw anytime, unlike CDs

- Interest paid monthly and compounded daily

It’s not a special investment. It’s not risky. It’s just a regular savings account at a bank that pays a competitive rate.

Why the Timing Matters Right Now

A quick market note. The Federal Reserve is currently holding the federal funds rate at 3.50 to 3.75 percent (as of July 2026), and observers expect them to hold steady for the rest of the year. That means HYSA rates are stable in the 3.50 to 4.20 percent range for now, but they typically drift down when the Fed cuts rates.

Translation: today’s rates are the good ones. Two years ago, the best HYSAs paid under 1 percent. Two years from now, nobody knows. Opening an account now locks in access to today’s higher rates. The interest rate itself will fluctuate over time (that’s normal for savings accounts), but the gap between your big bank and a good HYSA has stayed at 5 to 10 times higher for the last several years.

The Two-Account Strategy

This is the setup that works for almost everyone. Simple, low-friction, and it makes the whole system automatic.

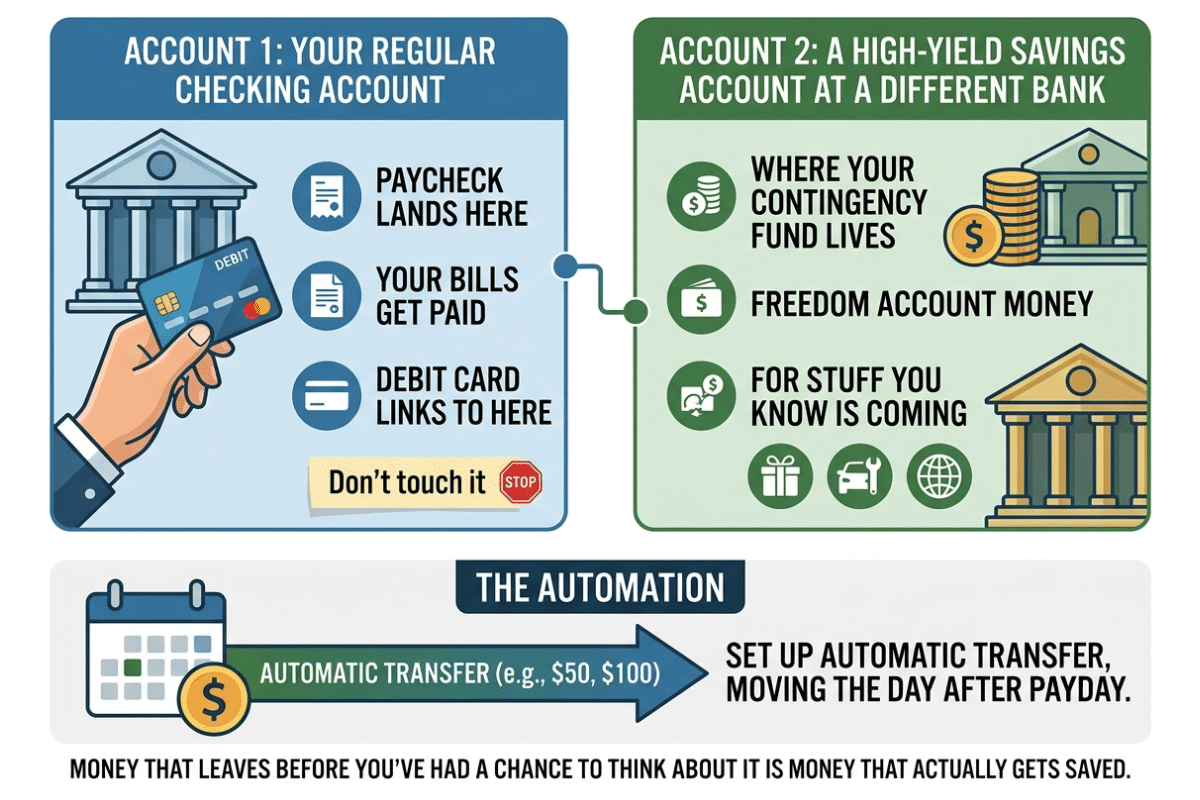

Account 1: Your Regular Checking Account

Keep this where it is. Your paycheck lands here. Your bills get paid from here. Your debit card links to here. This account exists for daily cash flow and immediate access.

Don’t touch it. You don’t need to overhaul your whole banking life to make this work.

Account 2: A High-Yield Savings Account at a Different Bank

Account two is your HYSA, at a different bank. This is where your Contingency Fund lives, along with your Freedom Account money for the stuff you know is coming: holiday spending, car repairs, that vacation you’re already dreaming about. Link it to your checking account and let the transfer time work for you. A day or two of friction between “I want to spend this” and “I can spend this” has saved me from myself more than once.

The Automation

Then set up an automatic transfer, even $50 or $100 a month, moving the day after payday. Money that leaves before you’ve had a chance to think about it is money that actually gets saved.

Who’s Worth Your Money Right Now (July 2026)

Rates change monthly, so the specific APY numbers below will shift over time. Always check the bank’s current rate before opening. That said, the players and their track records don’t move around much.

The Big-Name Reliable Choices

These are the online banks that have been around for years, are well-regarded, and consistently offer competitive (if not the absolute highest) rates. Any of these is a fine choice, and I wouldn’t talk you out of any of them.

- Ally Bank: No minimums, no fees, excellent app, buckets feature for organizing savings goals. Currently around 3.00% APY. My longtime personal pick for its simplicity. Learn more →

- Marcus by Goldman Sachs: No minimums, no fees, straightforward. Currently around 3.40% APY. Backed by Goldman Sachs, which is about as institutionally solid as it gets. Learn more →

- Capital One 360 Performance Savings: No minimums, no fees, and has physical cafes if you like occasional in-person access. Currently around 3.00% APY. Learn more →

- American Express High Yield Savings: No minimums, no fees, well-known brand. Currently around 3.00% APY. Great if you already have an Amex card. Learn more →

The Higher-Yield Options (With Caveats)

These banks currently offer slightly higher rates but come with more strings attached. Worth considering if you’re going to keep a larger balance.

- CIT Bank Platinum Savings: Currently around 3.75% APY, but requires a $5,000 minimum balance to earn the top rate. If your balance dips below, the rate drops sharply. Learn more →

- Forbright Bank Growth Savings: Currently around 3.85% APY, no minimum balance required. There’s also a promotional 4.15% rate for new customers through the end of 2026, but that one does require a $1,000 minimum. Learn more →

- E*TRADE Premium Savings: Currently around 3.50% APY. Good option if you already have an E*TRADE brokerage account. Learn more →

All-in-One Banking Options

These accounts combine checking and high-yield savings into a single relationship. Useful if you want to move your primary banking online.

- SoFi Checking & Savings: Currently around 3.80% APY on savings (with direct deposit), 0.50% on checking, no minimums, no fees. Learn more →

- Wealthfront Cash Account: Base rate is 3.30% APY, no minimum. You can stack that up to 4.20% by combining a 3-month new-client boost (+0.65%, capped at $150,000) with a permanent bump for direct depositing $1,000/month plus keeping a funded investing account (+0.25%). Technically a brokerage account, functions like a checking/savings hybrid. Learn more →

Your Local Credit Union (Don’t Skip This)

Credit unions occasionally offer surprisingly competitive rates on savings and money-market accounts, especially for members. Check what’s available at any credit union you already belong to. NCUA insurance is equivalent to FDIC.

What to Check Before You Open One

A few things worth thirty seconds of your time:

- Is it FDIC-insured? Non-negotiable. It should say so plainly on the site. If it doesn’t, walk away.

- Any hidden fees? Some charge for excess withdrawals or paper statements. Read the fee schedule once.

- Is there a minimum for the top rate? This is the oldest trick in the book. Below a certain balance, that shiny APY quietly disappears.

- Is the rate a teaser? Some accounts advertise a great rate for the first few months, then drop it. Read past the headline number.

- How fast are transfers, and how many are you allowed? For a Contingency Fund, quick access actually matters.

- Is the app any good? You’ll live in this app. A clunky one turns a smart money move into a chore you avoid.

How to Open One (It Takes 15 Minutes)

The process is genuinely simple:

- Pick a bank from the list above

- Go to their website and click “Open account”

- Provide your name, address, Social Security number, and driver’s license number

- Link your existing checking account (routing number and account number, easily found on any check or in your bank app)

- Fund the new account with an initial transfer

- Wait 2 to 5 business days for the account to be verified and funded

- Set up automatic monthly transfers from your checking account

The whole process takes about 15 minutes online. No credit check (opening a savings account doesn’t ping your credit). No paperwork by mail. No branch visit required.

Where This Fits in Your Financial Plan

A high-yield savings account is the right home for money that meets three criteria:

- You want it FDIC-insured and safe. No market risk.

- You need access to it within a year or two. Not money you’re locking away for retirement.

- You’re not planning to spend it in the next few weeks. Otherwise it can just stay in checking.

That covers your Contingency Fund, holiday savings, car repair money, home maintenance money, vacation savings, and quarterly tax savings if you’re self-employed. Basically, all the “I know this is coming” and “I hope this never comes” money most households carry around.

Money you’re not touching for five years or more, retirement, a kid’s college fund, a house down payment way out on the horizon, belongs somewhere else entirely: a retirement account, a 529, a taxable brokerage account. But your Contingency Fund and your Freedom Account? This is exactly where they should live.

The Real Return

Let’s do real math, because it’s more convincing than I am.

| Savings balance | At 0.38% | At 3.75% | Difference |

|---|---|---|---|

| $5,000 | $19/yr | $188/yr | $169/yr |

| $15,000 | $57/yr | $563/yr | $506/yr |

| $50,000 | $190/yr | $1,875/yr | $1,685/yr |

The math is the same for every household. The only variable is how much money you have in savings, and how long you’ve been leaving it in an account that doesn’t pay much. Every year of delay is real money left on the table.

The Fine Print

This is general information, not personalized financial advice for your specific situation. Rates move, banks change their offers, and everybody’s circumstances are a little different. Check current rates directly with the bank before you open anything, and if your finances are genuinely complicated, a fee-only planner is worth the conversation.

None of that changes the basic point, though. Moving idle cash from a 0.38 percent account into a 3.75 percent one is about as close to a free lunch as personal finance gets. It’s not clever. It’s just something worth actually doing, instead of meaning to do.

Question: Have you already made the switch? Tell me which bank you landed on and whether you’d still pick it today. And if you haven’t moved yet, what’s holding you back? Drop it in the comments. It helps everybody else reading this figure out where to start.

EverydayCheapskate™ is reader-supported. This post is general educational information, not personalized financial advice. Interest rates and account terms change frequently, so verify current rates directly with the bank before opening any account. All banks listed are FDIC-insured; confirm insurance status on each institution’s site.

More from Everyday Cheapskate

https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should)

https://www.everydaycheapskate.com/wp-content/uploads/20260711-estate-sale-what-to-buy-used-and-what-to-avoid.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-11 22:54:052026-07-11 22:54:057 Things to Always Buy Used (And 5 You Never Should) https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies)

https://www.everydaycheapskate.com/wp-content/uploads/20260710-luxury-car-driving-down-mountain-highway-how-to-lower-car-insurance-premium-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-10 17:46:132026-07-10 17:46:13How to Knock $200+ Off Your Car Insurance Bill (Without Switching Companies) https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50%

https://www.everydaycheapskate.com/wp-content/uploads/20260706-negotiate-medical-bills-female-nurse-with-calculator-and-ipad-negotiating-a-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-06 21:19:252026-07-06 21:19:25How to Negotiate Medical Bills and Cut Costs 30-50% https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom

https://www.everydaycheapskate.com/wp-content/uploads/20260704-financial-independence-sparkler-and-american-flag-in-night-sky.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-07-04 11:57:492026-07-04 11:57:49What My Debt Taught Me About Real Freedom https://www.everydaycheapskate.com/wp-content/uploads/20260617-how-to-build-a-1000-emergency-fund-jar-with-coins-and-plant.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-17 18:34:002026-06-17 18:34:00How to Build a $1,000 Emergency Fund When Money Is Already Tight

https://www.everydaycheapskate.com/wp-content/uploads/20260617-how-to-build-a-1000-emergency-fund-jar-with-coins-and-plant.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-17 18:34:002026-06-17 18:34:00How to Build a $1,000 Emergency Fund When Money Is Already Tight https://www.everydaycheapskate.com/wp-content/uploads/20260614-how-to-splurge-on-a-budget-woman-drinking-fancy-coffee-luxury-treat-smiling.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-14 20:10:232026-06-14 20:12:40How to Splurge on a Budget Without the Guilt

https://www.everydaycheapskate.com/wp-content/uploads/20260614-how-to-splurge-on-a-budget-woman-drinking-fancy-coffee-luxury-treat-smiling.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-14 20:10:232026-06-14 20:12:40How to Splurge on a Budget Without the Guilt https://www.everydaycheapskate.com/wp-content/uploads/20260607-woman-grocery-shopping-pushing-cart-with-apples-and-cauliflower.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-09 23:20:292026-06-09 23:20:29How to Read a Grocery Store Sale Cycle (And Stop Overpaying)

https://www.everydaycheapskate.com/wp-content/uploads/20260607-woman-grocery-shopping-pushing-cart-with-apples-and-cauliflower.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-09 23:20:292026-06-09 23:20:29How to Read a Grocery Store Sale Cycle (And Stop Overpaying) https://www.everydaycheapskate.com/wp-content/uploads/20260605-bill-glasses-and-pen-how-to-negotiate-your-cable-and-internet-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-05 10:07:222026-06-05 10:07:22The Word-For-Word Script That Cuts Your Bills by $600 a Year

https://www.everydaycheapskate.com/wp-content/uploads/20260605-bill-glasses-and-pen-how-to-negotiate-your-cable-and-internet-bill.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-06-05 10:07:222026-06-05 10:07:22The Word-For-Word Script That Cuts Your Bills by $600 a Year https://www.everydaycheapskate.com/wp-content/uploads/20260514-buy-now-pay-later-app-on-iphone-in-womans-hands.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-05-14 10:20:212026-05-14 10:20:23Is Buy Now Pay Later Risky? What the Data Reveals

https://www.everydaycheapskate.com/wp-content/uploads/20260514-buy-now-pay-later-app-on-iphone-in-womans-hands.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2026-05-14 10:20:212026-05-14 10:20:23Is Buy Now Pay Later Risky? What the Data Reveals

I have my HYSA at Alliant Credit Union. Easy to use app. New members who direct deposit at least $100 per month for the first 12 months get paid a bonus of $100 on top of the interest they have already earned. Interest rate is 3.01%. They also offer CD’s, Checking, etc.

THANK YOU THANK YOU THANK YOU!

As always, you made my life easier. I’ll get right on setting one of these up 🙂

You’re welcome! And thanks again for the suggestion.

I keep my savings with Apples savings plan with Goldman Saks. Has just dropped to 3.25% but still better than the banks.

I learned about these banks a few years ago and after doing the research signed up with UFB. It was easy to sign up and make transfers between accounts. We started earning $40 bucks a month interest instead of 40 cents a month. Thanks for all that you’ve taught me over the years from long distance calling cards to paying off debt to using Freedom accounts to how to clean filthy cabinets to making great iced tea! I am proud to say that we are debt free, our home is paid off and we have the peace of mind that comes with those things plus savings! We appreciate you!

I recently switched from Ally to LiveOak Bank. LiveOak is paying 3.8 %. I was shocked to find out that LiveOak only provides ATM cards to business accounts, but I’m making it work without one. If I have to, I’ll transfer money to my local fee-free, but also non-interest paying bank, and then make an ATM withdrawal from that account.

i kept hearing about money market accounts, but never looked into them. my CU explained & now instead of making $2/month on account, it’s closer to $22! they also routinely have short term (a few months) CD’s at great rates – 5K limit, but easy to work with, and gain a little extra in the bank. works for me!

My savings pays 3.40%, it’s Smarty Pig by Sallie Mae. I ❤️it FDIC Insured as wellz