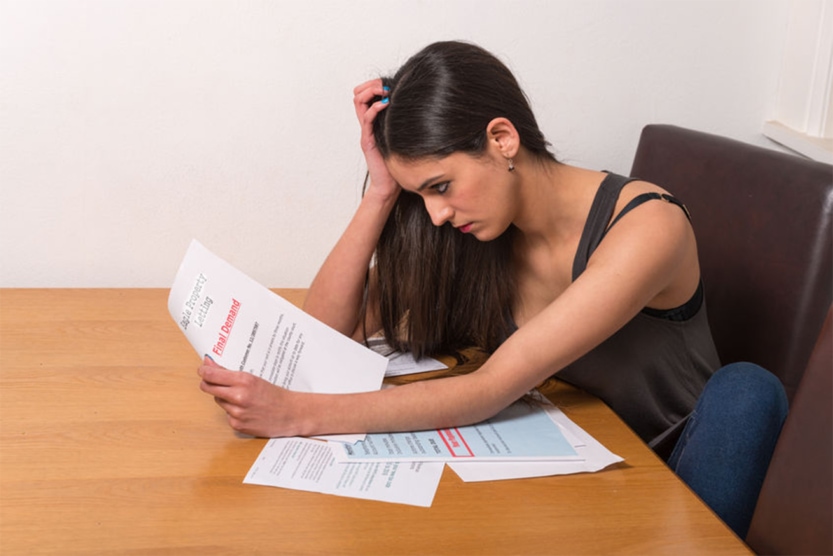

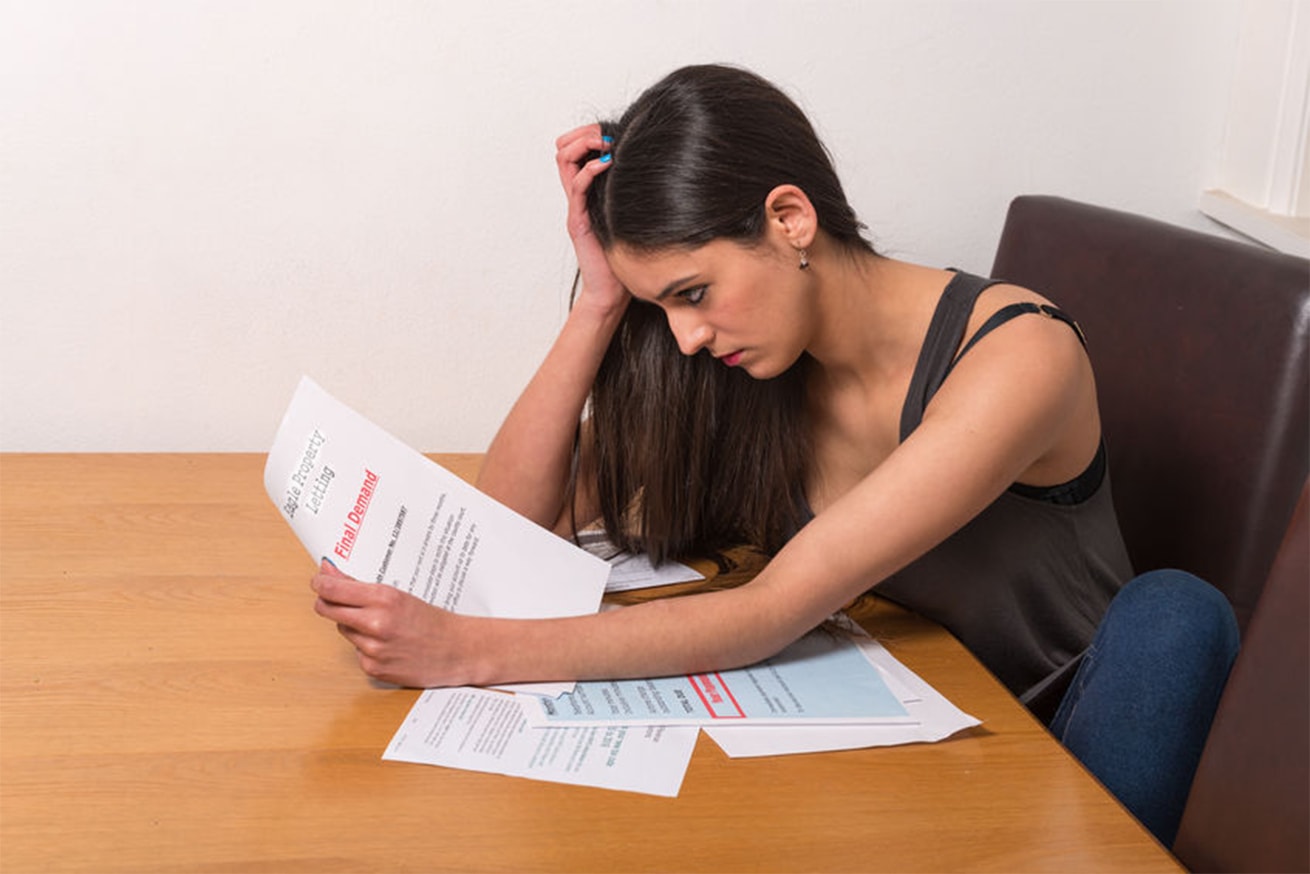

Top 10 Student Loan Tips for Recent Graduates and Not So Recent Too

Whether you just graduated, you’re taking a break from school, or have already started repaying your student loans, these tips will help you keep your student loan debt under control.

By “under control” I’m talking about:

- avoiding fees and extra interest costs

- keeping your payments affordable

- protecting your credit rating

- paying those loans in full as quickly as possible

If you’re having trouble finding a job or keeping up with your payments, there’s vitally important information here for you, too.

1. Know your loans

It’s crucial that you keep track of the lender, balance, and repayment status for each of your student loans. These details determine your options for loan repayment and possibilities for forgiveness.

If you’re not sure, ask your lender or visit StudentAid.gov. You can log in and see the loan amounts, lender(s), and repayment status for all of your federal loans.

In the event that some of your loans aren’t listed, they’re probably private (non-federal) loans. For those, try to find a recent billing statement or the original paperwork that you signed. Contact your school if you can’t locate any records.

2. Know your grace period

Different loans have different grace periods. A grace period is the amount of time between leaving school before you must make your first payment.

It’s six months for federal Stafford loans, but nine months for federal Perkins loans.

(Under federal law, the authority for schools to make new Perkins Loans ended on Sept. 30, 2017, and final disbursements were permitted through June 30, 2018. As a result, students can no longer receive Perkins Loans.)

For the federal parent or PLUS loans, there is no specified grace period. When payments begin depends on when the loans were issued (see specific details in your loan documents).

For loans first disbursed on or after July 1, 2008, parents may elect to postpone repayment until six months after the date that his or her child for whom the loan was borrowed ceases to be enrolled at least half-time. A parent PLUS borrower will have two options available to begin repayment:

- Within 60 days after the loan is fully disbursed; or

- Postpone repayment of principal for the day after 6 months following the date the dependent student for whom the loan was borrowed ceases to be enrolled at least half-time.

The grace periods for private student loans vary, so consult your paperwork or contact your lender to find out. Don’t miss your first payment.

3. Stay in touch with your lender

Whenever you move or change your phone number or email address, tell your lender right away. If your lender needs to contact you and your information isn’t current, it can end up costing you a bundle.

Open and read every piece of mail―paper or electronic―that you receive about your student loans. If you’re getting unwanted calls from your lender or a collection agency, don’t stick your head in the sand.

Talk to your lender. Lenders are supposed to work with borrowers to resolve problems, and collection agencies have to follow certain rules. Ignoring bills or serious problems can lead to default, which has severe, long-term consequences (see Tip 6 for more about default).

4. Pick the right repayment option

When your federal loans come due, your loan payments will automatically be based on a standard 10-year repayment plan, although there will be no prepayment penalty if you speed the repayment process by doubling up on payments or paying down big chunks of the principal ahead of time.

If the standard payment is going to be difficult for you to cover, there are other options, and you can change plans down the line if you want or need to.

Extending your repayment period beyond 10 years can lower your monthly payments, but you’ll end up paying more interest―often a lot more―over the life of the loan. You will live to regret that decision.

One option is the Income-Based Repayment (IBR) program. It can cap your monthly payments at a reasonable percentage of your income each year, and forgive any debt remaining after 25 years of affordable and on-time payments. Forgiveness may be available after just 10 years of these payments for borrowers in the public and nonprofit sectors (see Tip 10).

To find out more about Income-Based Repayment and how it might work for you, see How Is Income-Based Repayment Calculated?

NOTE: Private student loans are not eligible for IBR or the other federal loan payment plans, deferments, forbearances, or forgiveness programs. However, the lender may offer some type of forbearance, typically for a fee.

Read your original private loan paperwork carefully and then talk to the lender about what repayment options you may have.

5. Don’t panic

If you’re having trouble making payments because of unemployment, health problems, or other unexpected financial challenges, remember that you have options for managing your federal student loans.

There are legitimate ways to temporarily postpone your federal loan payments, such as deferments and forbearance. Just keep in mind that the interest will continue to accrue and be added to the principal amount, even though your payments may have been suspended.

For example, an unemployment deferment might be the right choice for you if you’re having trouble finding work right now. Again, beware: Interest accrues on all types of loans during forbearances, and on some types of loans during deferment, increasing your total debt. Ask your lender about making interest-only payments if you can afford it.

If you expect your income to be lower than you’d hoped for more than a few months, check out Income-Based Repayment. Your required payment in IBR can be as little as $0 when your income is very low. Refer back to Tip 4 for more about IBR and other repayment options.

6. Stay out of trouble

Ignoring your student loans has serious consequences that can last a lifetime. Not paying can lead to delinquency and default. For federal loans, default kicks in after nine months of non-payment.

When you default, your total loan balance becomes due, your credit score is ruined, the total amount you owe increases dramatically, and the government can garnish your wages and seize your tax refunds and eventually your Social Security benefits if you default on a federal loan.

- YIKES: 3 million senior citizens in the U.S. are still paying off their student loans

For private loans, a default can happen much more quickly and can put anyone who cosigned for your loan at risk as well.

Talk to your lender right away if you’re in danger of default. You can also find helpful information at StudentAid.gov.

7. Lower the principal

When you make a federal student loan payment, it covers any late fees first, then interest, and finally the principal. If you can afford to pay more than your required monthly payment―even occasionally―you can lower your principal, which reduces the amount of interest you have to pay over the life of the loan.

Include a written request to your lender to make sure that the extra amount is applied to your principal. Otherwise, it will automatically be applied to future interest payments instead.

Keep copies for your records and check back to be sure the overpayment was applied correctly.

8. Pay off most expensive loans first

If you’re considering paying off one or more of your loans ahead of schedule or trying to reduce the principal, start with the one that has the highest interest rate. If you have private loans in addition to federal loans, start with your private loans, since they almost always have higher interest rates and lack the flexible repayment options and other protections of federal loans.

9. To consolidate or not to consolidate

A consolidation loan combines multiple loans into one for a single monthly payment and one fixed interest rate. If this is appealing, make sure you know all of the pros and cons first, before you consolidate. You can consolidate your federal student loans through the Direct Loan program, and this calculator can help you figure out what your interest rate would be.

For private consolidation loans, shop around carefully for a low or fixed interest rate if you can find one, and read all the fine print.

Never consolidate federal loans into a private student loan (or even a home equity or other non-student loan), or you’ll lose all the repayment options and borrower benefits―like unemployment deferments and loan forgiveness programs―that come with federal loans.

10. Student loan forgiveness

There are various programs purporting to forgive all or some of your federal student loans if you work in certain fields or for certain types of employers. The operative word being: purport.

Public Service Loan Forgiveness is a fairly new federal program that forgives any student debt remaining after 10 years of qualifying payments for people in government, nonprofit, and other public service jobs. And there’s a lot of misinformation out there making forgiveness appear to be a viable option for just about anyone.

How many student loan borrowers were forgiven? Since the program began, 99% of the applications have been rejected. Find out more at IBRinfo.org.

Best advice: Don’t count on your loans to be forgiven, canceled, or paid off for you. However, an astonishing act of kindness would be amazing, right?

There are other federal loan forgiveness options available for teachers, nurses, Ameri-Corps and PeaceCorps volunteers, and other professions, as well as some state, school, and private programs. If you fall into any of those categories, do some research! It could pay off well for you.

More from Everyday Cheapskate

https://www.everydaycheapskate.com/wp-content/uploads/20240421-a-homemade-frittata-in-a-cast-iron-skillet.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-21 00:40:452024-04-09 12:56:11What’s Better and Cheaper Than Eating Out? A Fabulous Frittata!

https://www.everydaycheapskate.com/wp-content/uploads/20240421-a-homemade-frittata-in-a-cast-iron-skillet.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-21 00:40:452024-04-09 12:56:11What’s Better and Cheaper Than Eating Out? A Fabulous Frittata! https://www.everydaycheapskate.com/wp-content/uploads/20240422-best-liege-belgian-waffle-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-20 08:25:002024-04-21 17:16:07From Brussels with Love: How to Make Authentic Liège Waffles at Home

https://www.everydaycheapskate.com/wp-content/uploads/20240422-best-liege-belgian-waffle-.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-20 08:25:002024-04-21 17:16:07From Brussels with Love: How to Make Authentic Liège Waffles at Home https://www.everydaycheapskate.com/wp-content/uploads/20240420-house-guest-room-bright-white-walls-light-window-houseplant-bed.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-20 00:39:192024-04-07 15:48:43How to Be a Good House Guest Worthy of a Repeat Invitation in the Future

https://www.everydaycheapskate.com/wp-content/uploads/20240420-house-guest-room-bright-white-walls-light-window-houseplant-bed.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-20 00:39:192024-04-07 15:48:43How to Be a Good House Guest Worthy of a Repeat Invitation in the Future https://www.everydaycheapskate.com/wp-content/uploads/20240419-DIY-dusting-spray-womans-hand-wiping-dusty-wood-surface-with-yellow-towel.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-19 00:48:462021-04-23 12:16:59How to DIY Highly Effective Dusting Spray: Safe on Fine Wood Furniture

https://www.everydaycheapskate.com/wp-content/uploads/20240419-DIY-dusting-spray-womans-hand-wiping-dusty-wood-surface-with-yellow-towel.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-19 00:48:462021-04-23 12:16:59How to DIY Highly Effective Dusting Spray: Safe on Fine Wood Furniture https://www.everydaycheapskate.com/wp-content/uploads/20240418-mothers-day-brunch-overhead-view-scones-bread-fruit-coffee.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-18 00:39:222024-04-18 13:57:47How to Plan, Prepare, and Host the Perfect Mother’s Day Brunch at Home

https://www.everydaycheapskate.com/wp-content/uploads/20240418-mothers-day-brunch-overhead-view-scones-bread-fruit-coffee.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-18 00:39:222024-04-18 13:57:47How to Plan, Prepare, and Host the Perfect Mother’s Day Brunch at Home https://www.everydaycheapskate.com/wp-content/uploads/20240414-a-fiddle-leaf-fig-whose-leaves-are-made-out-of-dollar-bills-in-a-midcentury-home-low-risk-investment.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-14 00:05:112024-04-13 14:58:27The Ultimate High-Yield, Guaranteed, Risk-Free Investment

https://www.everydaycheapskate.com/wp-content/uploads/20240414-a-fiddle-leaf-fig-whose-leaves-are-made-out-of-dollar-bills-in-a-midcentury-home-low-risk-investment.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-14 00:05:112024-04-13 14:58:27The Ultimate High-Yield, Guaranteed, Risk-Free Investment https://www.everydaycheapskate.com/wp-content/uploads/20240409-companion-planting-calendula-and-tomato-plants.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-09 00:33:482024-04-06 12:55:08Natural Pest Control: Companion Planting Strategies for Your Frugal Garden

https://www.everydaycheapskate.com/wp-content/uploads/20240409-companion-planting-calendula-and-tomato-plants.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-09 00:33:482024-04-06 12:55:08Natural Pest Control: Companion Planting Strategies for Your Frugal Garden https://www.everydaycheapskate.com/wp-content/uploads/20240404-midcentury-modern-bathroom-clean-bathroom.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-04 00:42:322024-03-26 22:52:43The Ultimate Step By Step Guide to a Clean Bathroom in 15 Minutes

https://www.everydaycheapskate.com/wp-content/uploads/20240404-midcentury-modern-bathroom-clean-bathroom.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-04 00:42:322024-03-26 22:52:43The Ultimate Step By Step Guide to a Clean Bathroom in 15 Minutes https://www.everydaycheapskate.com/wp-content/uploads/20240401-laptop-with-chalkboard-with-hot-deals-april-2024-piece-of-chalk-best-deals.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-01 00:48:282024-04-22 21:38:48Hot Deals • April 2024

https://www.everydaycheapskate.com/wp-content/uploads/20240401-laptop-with-chalkboard-with-hot-deals-april-2024-piece-of-chalk-best-deals.png

800

1200

Mary Hunt

https://www.everydaycheapskate.com/wp-content/uploads/EC-Logo-by-Mary-Hunt-Tagline-Trimmed.png

Mary Hunt2024-04-01 00:48:282024-04-22 21:38:48Hot Deals • April 2024

Thank goodness I got Pell Grants to cover my college. My granddaughter has money from her great grandfather that is going to pay for her college, same with my grandson.

College tuition has gone up so much, you’d be lucky if a Pell Grant covered half of your tuition/fees at a traditional 4 year public university. The maximum amount you can get for a Pell Grant is $6,345 per year, while the average tuition of a public university is close to 10 grand (not including fees or living costs).